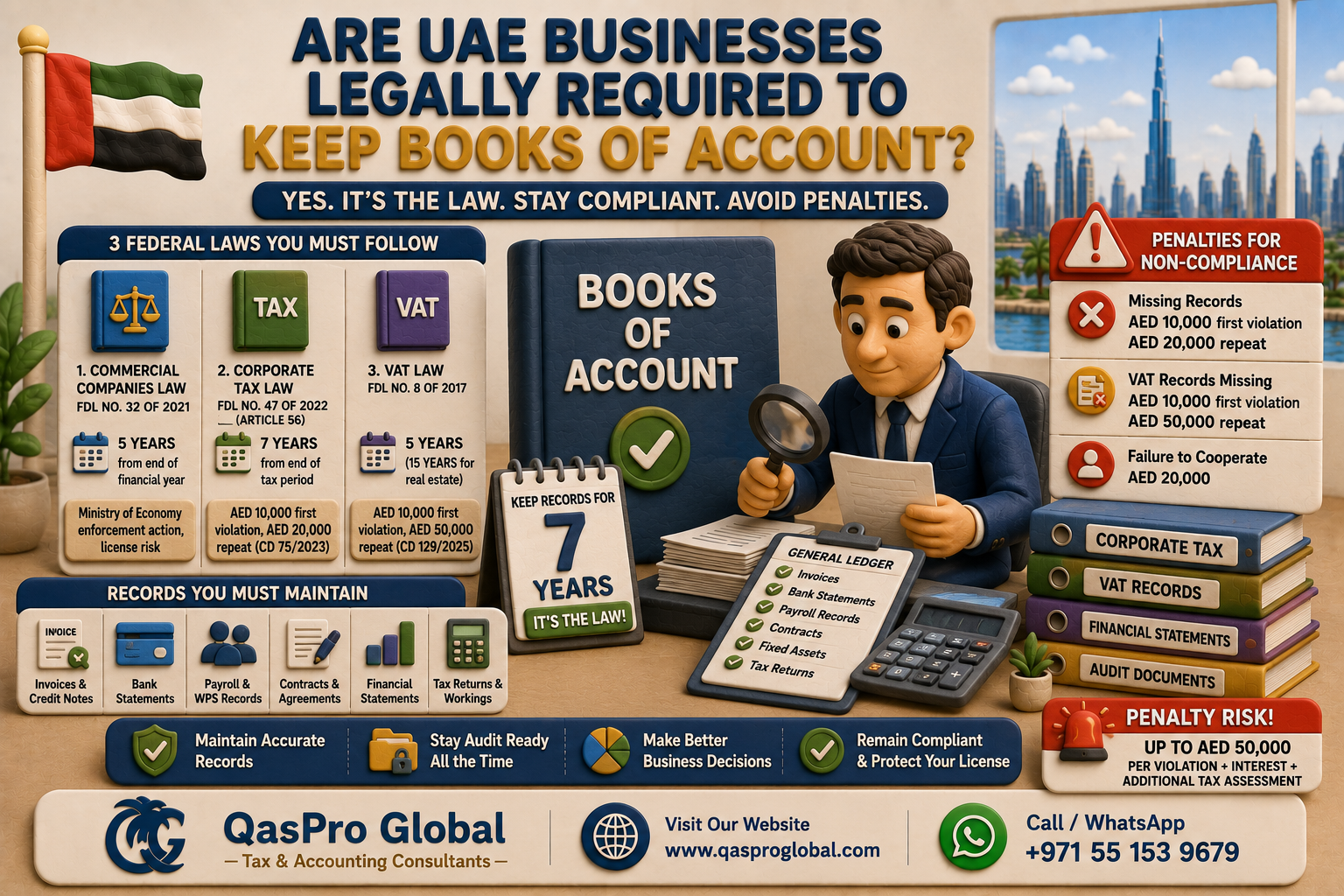

Are UAE Businesses Legally Required to Keep Books of Account?

Yes. Every business operating in the UAE, mainland or free zone, sole proprietor or LLC, is legally required to maintain proper books of account under three separate federal laws. This is not just a tax requirement. It is a corporate governance obligation that predates the introduction of Corporate Tax and VAT. In 2026, with the FTA conducting more audits than ever before, failure to maintain compliant records triggers penalties starting at AED 10,000 per violation under Cabinet Decision 75 of 2023.

In this guide, Qaspro Global breaks down each law, the specific records it requires, how long you must keep them, and what the FTA will look for if your business is selected for audit.

What Are the 3 Federal Laws That Govern UAE Accounting and Bookkeeping Regulations?

UAE businesses must comply with three separate federal laws on recordkeeping, each with different requirements and retention periods. Understanding which law applies to your business and what it demands is the starting point for accounting compliance in 2026.

| Law | Applies To | Retention Period | Penalty for Non-Compliance |

|---|---|---|---|

| Federal Decree-Law No. 32 of 2021 (Commercial Companies Law) | All registered companies | 5 years from end of financial year | Ministry of Economy enforcement action, license risk |

| Federal Decree-Law No. 47 of 2022 (Corporate Tax Law, Article 56) | All taxable persons | 7 years from end of tax period | AED 10,000 first violation, AED 20,000 repeat (CD 75/2023) |

| Federal Decree-Law No. 8 of 2017 (VAT Law) | VAT-registered businesses | 5 years (15 years for real estate) | AED 10,000 first violation, AED 50,000 repeat (CD 129/2025) |

If your business is VAT-registered and subject to Corporate Tax, all three laws apply simultaneously. The longest retention period governs: you must keep all records for at least 7 years.

Law 1: Commercial Companies Law (Federal Decree-Law No. 32 of 2021)

Article 26 of Federal Decree-Law No. 32 of 2021 requires every registered company in the UAE to maintain accurate books of account that correctly reflect its financial transactions and position. This obligation exists independently of tax compliance and predates the introduction of Corporate Tax.

What Article 26 Requires

- Maintain books of account that accurately reflect all transactions and the financial position of the company

- Retain records for at least 5 years from the end of each financial year

- Prepare financial statements using internationally recognised accounting standards (IFRS)

- Make records available for inspection by the Ministry of Economy or the relevant free zone authority on request

This applies to LLCs, public joint stock companies, private joint stock companies, and most free zone entities. Sole proprietors are not technically commercial companies under this law, but they remain fully subject to the Corporate Tax Law and VAT Law requirements below.

Law 2: Corporate Tax Law (Federal Decree-Law No. 47 of 2022)

Article 56 of Federal Decree-Law No. 47 of 2022 sets the strictest bookkeeping requirement of the three laws. Every taxable person must maintain all records and documents for a period of 7 years following the end of the tax period to which they relate. This 7-year requirement applies whether or not a Corporate Tax Return shows any liability.

What Article 56 Requires

- All records and documents that support information provided in the Corporate Tax Return

- All records that enable Taxable Income to be readily ascertained by the FTA at any time

- Transfer pricing documentation for related-party and connected-person transactions (Article 55)

- Financial statements used to determine Taxable Income (Article 54)

- Records supporting any tax credits claimed, including Withholding Tax Credit and Foreign Tax Credit under Articles 46 and 47

The 7-year retention period overrides the shorter periods in the other two laws. If your business is subject to Corporate Tax, your entire bookkeeping baseline becomes 7 years from the end of each tax period.

What Accounting Standard Must You Use for Corporate Tax?

Ministerial Decision No. 114 of 2023 specifies three tiers of accounting standards based on annual revenue:

- IFRS (full International Financial Reporting Standards): mandatory for all taxable persons with revenue above AED 50,000,000

- IFRS for SMEs: permitted for businesses with revenue of AED 50,000,000 or below

- Cash basis of accounting: permitted only for businesses with revenue not exceeding AED 3,000,000

Once you select an accounting standard, you must apply it consistently. Switching between standards without FTA approval can result in restated financials and a penalty exposure for an incorrect Tax Return.

Who Must Prepare Audited Financial Statements?

Ministerial Decision No. 84 of 2025 (effective 25 March 2025, applying to tax periods commencing on or after 1 January 2025) requires the following to prepare and maintain audited financial statements:

- Any taxable person (not a Tax Group) with revenue exceeding AED 50,000,000 during the relevant tax period

- All Qualifying Free Zone Persons (QFZPs), regardless of revenue

- Tax Groups (required to prepare audited special purpose consolidated financial statements)

If your free zone company claims the 0% QFZP corporate tax rate, you are automatically required to maintain audited financial statements for every tax period from 1 January 2025 onwards. There is no revenue threshold exemption for QFZPs. This is a hard requirement under MD 84/2025 Article 2 and applies even if your annual revenue is AED 100,000.

Law 3: VAT Law (Federal Decree-Law No. 8 of 2017)

VAT-registered businesses are subject to a parallel set of bookkeeping obligations under the UAE VAT Law and its Executive Regulation. The standard retention period is 5 years from the end of the tax period to which each record relates.

What Records Are Required Under UAE VAT Law?

- All tax invoices issued to customers and received from suppliers

- All credit notes and debit notes

- Import and export records, including customs documentation

- Accounting records showing all taxable, exempt, and zero-rated supplies

- VAT Return workings and apportionment calculations

- Bank statements corroborating declared turnover

- Records of Designated Zone movements (if applicable)

The 15-Year Exception for Real Estate

Businesses involved in real estate transactions face a significantly longer retention requirement. Records relating to real estate supplies must be maintained for 15 years from the end of the tax period in which the transaction occurred. This applies to property developers, investors supplying commercial real estate, and businesses with taxable real estate dealings.

What Records Must Every UAE Business Maintain?

Regardless of which laws apply, the FTA expects to find the following records during any inspection. Missing records are treated as a failure to comply with Article 56 of the Corporate Tax Law, triggering the AED 10,000 penalty per violation.

Financial Records

- General ledger with all journal entries and postings

- Trial balance and chart of accounts

- Bank statements reconciled to the general ledger (monthly)

- Profit and loss statement (income statement)

- Balance sheet as at the financial year end

- Cash flow statement

Supporting Documents

- All purchase invoices and vendor bills

- All sales invoices issued to customers

- Payroll records, WPS salary reports, and bank transfer confirmations

- Lease agreements and rental contracts

- Fixed asset registers and depreciation schedules

- Loan agreements and interest calculations

- Related-party transaction records supported at arm’s length

Corporate Tax Specific Records

- Corporate Tax Return filed on EmaraTax

- Taxable Income calculation workings and adjustments

- Documentation for any claimed exemptions, reliefs, or elections

- Transfer pricing master file and local file (if applicable to your group)

- Documentation for Small Business Relief eligibility (if claimed)

- Foreign Tax Credit supporting calculations and foreign tax certificates

How Long Must UAE Businesses Keep Financial Records?

Retention periods differ by law. Since most UAE businesses are subject to all three frameworks, the safest approach is to apply the longest period (7 years) to all records. Here is the breakdown by record type:

| Record Type | VAT Law | CT Law (Art. 56) | Companies Law | Effective Minimum |

|---|---|---|---|---|

| Tax invoices and VAT records | 5 years | 7 years | 5 years | 7 years |

| Financial statements and accounts | 5 years | 7 years | 5 years | 7 years |

| Corporate Tax Return and workings | N/A | 7 years | N/A | 7 years |

| Payroll and WPS records | 5 years | 7 years | 5 years | 7 years |

| Real estate transaction records | 15 years | 7 years | 5 years | 15 years |

| Non-VAT registered companies (CT only) | N/A | 7 years | 5 years | 7 years |

Practical rule: keep everything for 7 years. If your business has real estate dealings, keep those specific records for 15 years. Cloud accounting software with automated backup is the most reliable way to ensure compliance without physical storage costs.

What Are the Penalties for Failing to Maintain Records in the UAE?

Qaspro Global advises all clients to treat record-keeping as a priority, not an afterthought. The FTA conducted 93,000 inspection visits in 2024, a 135% increase year-on-year. When records are missing or incomplete, the following penalties apply immediately.

Corporate Tax Penalties (Cabinet Decision 75 of 2023)

- AED 10,000 for each instance of failure to maintain required records or documents

- AED 20,000 for each repeated violation within 24 months of the previous penalty

- AED 5,000 for failure to provide records in Arabic when requested by the FTA

- AED 20,000 for failure to cooperate with or facilitate a Tax Auditor (non-cooperation penalty)

VAT Penalties (Cabinet Decision 129 of 2025)

- AED 10,000 for the first instance of failure to maintain required VAT records

- AED 50,000 for a repeated violation

These penalties are cumulative. If the FTA finds that both VAT records and CT records are incomplete in the same audit, both penalty schedules apply. A business with two sets of missing records can face AED 60,000 in penalties from a single inspection, before any tax assessment on unreported income.

Do UAE Bookkeeping Regulations Apply to Free Zone Companies?

Yes. Free zone companies are subject to all three federal laws. The Commercial Companies Law applies to free zone entities registered as legal persons under their respective free zone regulations. The Corporate Tax Law applies to all businesses in the UAE, including every free zone, from the first tax period commencing on or after 1 June 2023. The VAT Law applies to all VAT-registered businesses regardless of location.

Free zone companies claiming the 0% QFZP corporate tax rate face an additional obligation: they must prepare and maintain audited financial statements for every tax period under Ministerial Decision 84 of 2025. This is mandatory regardless of revenue size. A QFZP company with AED 300,000 in annual revenue must still have its accounts audited by an approved UAE auditor.

What Is Changing in Accounting Compliance in 2026 and 2027?

Two important developments affect UAE accounting compliance in the near term and require advance preparation.

IFRS 18 Replaces IAS 1 from 1 January 2027

IFRS 18 (Presentation and Disclosure in Financial Statements) replaces IAS 1 for financial years commencing on or after 1 January 2027. For UAE businesses on a January-December financial year, the 2026 financial statements will be the comparative baseline period when 2027 accounts are prepared under IFRS 18. Businesses should begin aligning their income statement presentation and management performance disclosures to IFRS 18 requirements now, particularly around the new classification of operating, investing, and financing categories.

Mandatory E-Invoicing from January 2027

UAE e-invoicing under Ministerial Decisions 243 and 244 of 2025 becomes mandatory from January 2027 for Phase 1 businesses with revenue above AED 50 million. The PINT AE structured digital format must be used via an FTA-accredited service provider. Any accounting or billing system that does not support the PINT AE format will create a compliance gap from January 2027, affecting your ability to issue valid VAT invoices and maintain compliant records under the VAT Law.

Frequently Asked Questions

Is bookkeeping mandatory for all UAE businesses?

Yes. Every business registered in the UAE is legally required to maintain books of account under Federal Decree-Law No. 32 of 2021 (Commercial Companies Law). This applies to mainland companies, free zone entities, and businesses of all sizes. Corporate Tax and VAT laws impose further record-keeping obligations on top of this baseline requirement.

How long do UAE businesses need to keep accounting records?

The minimum is 5 years under the Commercial Companies Law and VAT Law, and 7 years under the Corporate Tax Law (Article 56 of Federal Decree-Law No. 47 of 2022). Businesses subject to Corporate Tax must keep all financial records for at least 7 years from the end of each tax period. Real estate transaction records must be kept for 15 years under UAE VAT regulations.

What accounting standard must UAE businesses use?

Under Ministerial Decision No. 114 of 2023, all taxable persons must use full IFRS by default. Businesses with revenue not exceeding AED 50 million may apply IFRS for SMEs. Businesses with revenue not exceeding AED 3 million may use cash basis accounting. The chosen standard must be applied consistently across all tax periods.

Which UAE businesses must prepare audited financial statements?

Under Ministerial Decision No. 84 of 2025 (effective for tax periods from 1 January 2025), audited financial statements are mandatory for taxable persons with revenue exceeding AED 50 million, all Qualifying Free Zone Persons regardless of revenue, and Tax Groups. QFZPs must have audited accounts even if annual revenue is below AED 1 million.

What is the penalty for not keeping accounting records in UAE?

Under Cabinet Decision 75 of 2023, the FTA imposes AED 10,000 for the first instance of failure to maintain required Corporate Tax records, and AED 20,000 for each repeated violation within 24 months. Separate VAT record-keeping penalties apply under Cabinet Decision 129 of 2025: AED 10,000 for first violation and AED 50,000 for repeat violations.

Do free zone companies need to comply with UAE bookkeeping laws?

Yes. Free zone companies are subject to all UAE federal bookkeeping requirements. Free zone companies claiming the 0% QFZP corporate tax rate must also prepare and maintain audited financial statements under Ministerial Decision 84 of 2025, effective from 1 January 2025, regardless of their revenue level.

Can UAE businesses store accounting records electronically?

Yes. The FTA accepts electronic records provided they are complete, accessible, and can be produced in Arabic when requested. Failure to provide records in Arabic when the FTA requests them attracts a separate AED 5,000 penalty under Cabinet Decision 75 of 2023. Cloud accounting software with regular backups is the recommended approach for most UAE businesses.

What happens to bookkeeping obligations when a company is deregistered?

Record-keeping obligations survive company deregistration. Under Article 56 of the Corporate Tax Law, records must be maintained for 7 years from the end of the tax period they relate to, regardless of whether the company remains active. Former directors and shareholders should ensure access to records is preserved for the full retention period after deregistration.

What does the FTA examine during a bookkeeping audit?

The FTA typically requests the general ledger, trial balance, bank statements reconciled to accounts, all purchase and sales invoices, payroll records, VAT Return workings, and Corporate Tax Return supporting documents. Missing or incomplete records trigger AED 10,000 per violation under Article 56 of the Corporate Tax Law, with each missing category counted as a separate violation.

How will IFRS 18 affect UAE bookkeeping in 2027?

IFRS 18 replaces IAS 1 for financial years starting on or after 1 January 2027. For businesses on a calendar financial year, the 2026 figures become the comparative baseline in the first IFRS 18 financial statements. Businesses should review the new income statement classification requirements under IFRS 18 and discuss the transition with their accountant or auditor before the 2026 year end to avoid restatement complications.

Need Expert Help With UAE Accounting Compliance?

Qaspro Global’s team of accountants and tax consultants provides bookkeeping, IFRS-compliant financial statement preparation, and audit coordination for businesses across all UAE jurisdictions. Whether you need compliant records for a Corporate Tax filing, an audit for QFZP status, or help organising your accounts before an FTA inspection, contact us today for a free consultation. WhatsApp: +971 55 153 9679.