Is All Your Bank Loan Interest Actually Deductible Under UAE Corporate Tax?

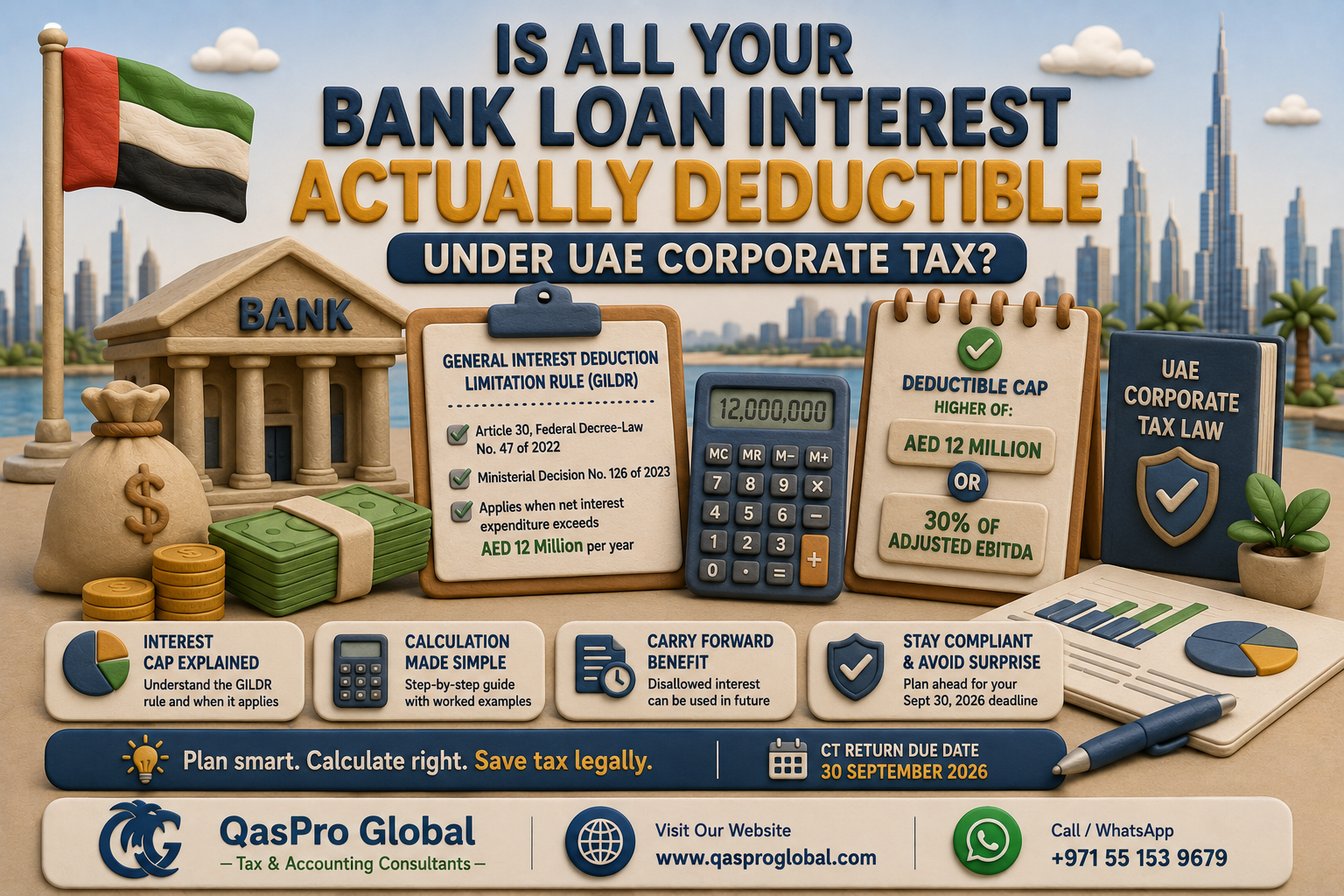

In this guide, Qaspro Global breaks down the UAE corporate tax interest deduction cap, known officially as the General Interest Deduction Limitation Rule (GILDR). If your business has bank loans, Islamic finance facilities, finance leases, or intercompany borrowings, this rule under Article 30 of Federal Decree-Law No. 47 of 2022 and Ministerial Decision No. 126 of 2023 directly affects how much interest you can deduct from your taxable income before the September 30, 2026 filing deadline.

Quick answer: Most UAE SMEs are completely safe because the rule only activates when net interest expenditure exceeds AED 12 million per year. But if your business carries significant debt, the GILDR cap can block part of your interest deduction and add an unexpected corporate tax bill of 9% on the disallowed portion.

What Is the General Interest Deduction Limitation Rule (GILDR)?

The General Interest Deduction Limitation Rule is the mechanism under Article 30 of Federal Decree-Law No. 47 of 2022 that caps how much net interest expenditure a UAE business can deduct against taxable income. The rule was introduced to prevent businesses from loading up on debt purely to reduce taxable profits. The full implementation rules are set out in Ministerial Decision No. 126 of 2023, issued by the Minister of State for Financial Affairs on 23 May 2023. For cryptocurrency and digital asset scenarios, see our guide on crypto lending and borrowing businesses.

Net interest expenditure means total interest paid minus total interest received in a tax period. If your business paid AED 20 million in loan interest but received AED 2 million in deposit interest, your net interest expenditure is AED 18 million. Whether the cap applies depends entirely on whether that figure crosses the AED 12 million threshold.

Who Does the UAE CT Interest Deduction Cap Apply To?

The GILDR applies to all UAE resident taxable persons subject to corporate tax, including mainland companies, free zone persons operating a mainland activity, and branches of foreign companies. However, several categories are exempt from the rule entirely:

- Banks and insurance companies: regulated financial institutions are excluded from GILDR by the nature of their business (Article 12, MD 126/2023)

- Qualifying Infrastructure Project Persons: businesses responsible for UAE public infrastructure (transport, utilities, education, healthcare) where assets last 10 or more years and are situated within UAE territory (Article 14, MD 126/2023)

- Historical financial liabilities: debt instruments with terms agreed before 9 December 2022 are grandfathered and exempt from GILDR for the net interest expenditure they generate (Article 11, MD 126/2023)

- Businesses below the de minimis threshold: if net interest expenditure is AED 12 million or less per tax period, the cap does not apply at all (Article 8, MD 126/2023)

For the vast majority of UAE businesses, the AED 12 million de minimis means the GILDR is simply not relevant. A business would need to carry roughly AED 150-200 million of bank debt at a 6-8% interest rate before approaching the threshold.

What Counts as “Interest” Under the UAE Corporate Tax Rules?

Ministerial Decision No. 126 of 2023 defines interest very broadly for GILDR purposes. It covers any financial return economically equivalent to interest, regardless of how it is named or classified in the accounts. The following all count as interest under the rule:

- Interest on bank loans and credit facilities, both performing and non-performing (Article 2)

- Interest-equivalent returns on Islamic financial instruments including Murabaha, Ijara, Wakala, and Sukuk (Article 4)

- Finance element of finance leases and non-finance leases (Article 5)

- Arrangement fees, guarantee fees, and commitment fees paid on financing facilities (Article 3)

- Interest components of forward contracts, futures, options, and FX swaps used to hedge financing risks (Article 3)

- Foreign exchange gains and losses accruing from interest positions (Article 6)

- Capitalised interest, recognised in the GILDR calculation when the capitalised amount is amortised, not when first incurred (Article 7)

- Interest components of factoring, securitisations, and repurchase agreements (Article 2)

Two points stand out for UAE businesses. First, if your company uses Islamic banking products, those returns count as interest for GILDR even though they are not called interest. Second, if you have IFRS 16 right-of-use assets with a finance cost element in your P&L, those costs feed into your net interest expenditure calculation under Article 5.

How to Calculate the UAE CT Interest Deduction Cap

The calculation follows three steps under Article 8 and Article 9 of Ministerial Decision No. 126 of 2023:

Step 1: Calculate Net Interest Expenditure (NIE) = total interest paid minus total interest received.

Step 2: Check the de minimis threshold. If NIE is AED 12 million or less, stop. No cap applies and the full amount is deductible.

Step 3: If NIE exceeds AED 12 million, calculate the deductible cap as the higher of:

- AED 12,000,000 (the de minimis floor), or

- 30% of Adjusted EBITDA for the tax period

Any NIE above the deductible cap is disallowed for the current year but carries forward to future tax periods, where it can be deducted subject to the cap applying again in those years.

How Is Adjusted EBITDA Calculated for GILDR Purposes?

The Adjusted EBITDA for GILDR is not simply your accounting EBITDA. Under Article 9 of Ministerial Decision No. 126 of 2023, it equals the greater of AED 0 or the following sum:

- Taxable Income for the period (as calculated under Article 20 of Federal Decree-Law No. 47 of 2022)

- Plus Net Interest Expenditure for the period

- Plus Depreciation and amortisation taken into account in determining taxable income

- Plus Interest income or expenditure on financial assets or liabilities held before 9 December 2022

Interest income and expenditure relating to Qualifying Infrastructure Projects are excluded from this EBITDA calculation. The adjusted EBITDA cannot fall below AED 0, which prevents negative EBITDA from creating a perverse result in the 30% calculation.

UAE CT Interest Deduction Cap: Two Worked Examples with AED Figures

Qaspro Global illustrates the GILDR calculation with two scenarios that show how the cap and the floor interact in practice.

Example 1: High-EBITDA business where the 30% formula applies

| Item | Amount (AED) |

|---|---|

| Total interest paid on bank loans | 20,000,000 |

| Total interest received on deposits | 2,000,000 |

| Net Interest Expenditure (NIE) | 18,000,000 |

| Exceeds de minimis of AED 12M? | Yes – cap applies |

| Adjusted EBITDA | 50,000,000 |

| 30% of Adjusted EBITDA | 15,000,000 |

| Higher of: AED 15M (30% EBITDA) or AED 12M (de minimis) | 15,000,000 |

| Deductible NIE | 15,000,000 |

| Disallowed NIE (carry forward) | 3,000,000 |

| Additional CT at 9% on disallowed amount | 270,000 |

Example 2: Lower-EBITDA business where the AED 12M floor protects the business

| Item | Amount (AED) |

|---|---|

| Net Interest Expenditure (NIE) | 18,000,000 |

| Adjusted EBITDA | 30,000,000 |

| 30% of Adjusted EBITDA | 9,000,000 |

| Higher of: AED 9M (30% EBITDA) or AED 12M (de minimis) | 12,000,000 |

| Deductible NIE | 12,000,000 |

| Disallowed NIE (carry forward) | 6,000,000 |

| Additional CT at 9% on disallowed amount | 540,000 |

In Example 2, the 30% EBITDA formula gives only AED 9 million, but the AED 12 million de minimis floor raises the deductible amount. This is why both figures must always be calculated. Businesses with lower EBITDA margins relative to their debt load benefit most from the de minimis floor.

What Happens to Disallowed Interest Under UAE Corporate Tax?

Disallowed net interest expenditure does not disappear permanently. Under Article 30 of Federal Decree-Law No. 47 of 2022, the excess NIE above the GILDR cap carries forward and can be deducted in future tax periods. The carry-forward deduction is subject to the GILDR cap applying again in those future years, meaning the business cannot deduct carried-forward NIE if it would push the total deduction above the applicable cap in the future year.

For businesses in a tax group, Ministerial Decision No. 126 of 2023 (Article 12) provides specific rules. When a subsidiary joins a group, its pre-grouping carried-forward NIE can only offset income attributable to that specific subsidiary within the group. When a subsidiary leaves, the group’s general carried-forward NIE stays with the group. If the parent company ceases to be a taxable person on dissolution of the group, the group’s carried-forward NIE generally cannot be inherited by individual subsidiaries, except for each subsidiary’s own pre-grouping amounts.

The Key Exemption for Loans Agreed Before 9 December 2022

Many UAE businesses entered into bank facilities and credit agreements before corporate tax was formally introduced on 9 December 2022. Article 11 of Ministerial Decision No. 126 of 2023 provides a grandfathering exemption: net interest expenditure attributable to debt instruments with terms agreed before 9 December 2022 is excluded from the GILDR calculation. The interest from those historical loans does not count towards the AED 12 million threshold and is fully deductible regardless of EBITDA.

The exemption only covers the original terms. If a pre-December 2022 loan is refinanced or its terms materially amended after that date, the exemption may be lost for the renegotiated portion. Businesses with legacy debt should document the original agreement date carefully, as the FTA may request evidence during a corporate tax audit.

GILDR and Islamic Finance: What UAE Businesses Need to Know

UAE businesses frequently use Sharia-compliant financing products. The GILDR treats these products identically to conventional debt for tax purposes. Under Article 4 of Ministerial Decision No. 126 of 2023, the interest-equivalent component on any Islamic financial instrument is treated as interest regardless of what the product is called. A Murabaha facility, an Ijara arrangement, or a Wakala structure will all have their profit rates or rental payments counted as interest expenditure in the NIE calculation if the economic substance is equivalent to conventional interest-bearing debt.

Steps UAE Businesses Should Take Before the September 30, 2026 CT Filing Deadline

For businesses with a financial year ending 31 December 2025, the corporate tax return must be filed by 30 September 2026. Qaspro Global recommends working through the GILDR calculation now, not at filing time:

- List all interest-bearing liabilities: bank loans, Islamic finance, finance leases, credit facilities, intercompany borrowings

- Check agreement dates: any debt with terms agreed before 9 December 2022 may be exempt from GILDR under Article 11

- Calculate total interest paid and interest received for the 2025 tax period to arrive at NIE

- Apply the de minimis check: if NIE is AED 12 million or less, the GILDR does not apply and interest is fully deductible

- If NIE exceeds AED 12M: calculate Adjusted EBITDA and apply the higher of AED 12M or 30% of EBITDA

- Record the disallowed NIE separately in your tax workings for carry-forward to the 2026 tax period

- Document everything: loan agreements, draw-down dates, Islamic finance agreements, lease contracts, and the EBITDA calculation should all be retained for potential FTA inspection

Late filing of the UAE corporate tax return costs AED 500 per month for the first year and AED 1,000 per month after that under Cabinet Decision No. 75 of 2023. Getting the interest deduction calculation right now avoids both underpayment penalties and costly amendments later.

How GILDR Interacts with Other UAE CT Deduction Rules

The GILDR works alongside, not instead of, the specific interest deduction limitation under Article 29 of Federal Decree-Law No. 47 of 2022. Article 29 is a separate rule that restricts interest deductions on intercompany loans where the purpose is to generate a deduction in the UAE without a corresponding taxable amount elsewhere (the anti-hybrid/anti-avoidance provision). A business may have some interest caught under Article 29 and additional interest caught under Article 30. Both sets of rules must be applied to arrive at the total deductible interest figure.

The GILDR also interacts with the depreciation rules under Ministerial Decision No. 173 of 2025, because depreciation and amortisation are added back when calculating the Adjusted EBITDA that drives the 30% cap. Higher depreciation charges increase the EBITDA base, which in turn increases the 30% cap and potentially allows more interest to be deducted. This creates a link between fixed asset investment decisions and the interest deduction position.

Frequently Asked Questions

What is the UAE corporate tax interest deduction cap?

The UAE corporate tax interest deduction cap is the General Interest Deduction Limitation Rule (GILDR) under Article 30 of Federal Decree-Law No. 47 of 2022. It limits deductible net interest expenditure to the higher of AED 12 million or 30% of adjusted EBITDA per tax period. Businesses with net interest expenditure of AED 12 million or less are completely exempt from the cap under Article 8 of Ministerial Decision No. 126 of 2023.

Does the GILDR apply to most UAE SMEs?

No. The GILDR has an AED 12 million de minimis threshold under Article 8 of Ministerial Decision No. 126 of 2023. A business would need roughly AED 150-200 million in outstanding bank debt at current interest rates before net interest expenditure approaches that threshold. The vast majority of UAE SMEs fall well below AED 12 million and face no restriction on their interest deductions.

Does Murabaha or Islamic finance count as interest for the GILDR?

Yes. Under Article 4 of Ministerial Decision No. 126 of 2023, the interest-equivalent component of Islamic financial instruments such as Murabaha, Ijara, Wakala, and Sukuk is treated as interest for GILDR purposes. The economic substance of the arrangement determines treatment, not the product name. Profit rates, rental payments, and similar returns on Islamic finance all feed into the net interest expenditure calculation.

Are finance lease payments subject to the UAE CT interest deduction cap?

Yes. Under Article 5 of Ministerial Decision No. 126 of 2023, the finance element of both finance leases and non-finance leases is treated as interest for GILDR purposes. If your business has IFRS 16 right-of-use assets with a finance cost component in the income statement, that cost forms part of your net interest expenditure and may be subject to the cap if the AED 12 million threshold is crossed.

What happens to UAE corporate tax interest that is not deductible in the current year?

Disallowed net interest expenditure carries forward under Article 30 of Federal Decree-Law No. 47 of 2022. It can offset taxable income in future tax periods, subject to the GILDR cap applying again in those years. The carry-forward is not time-limited in the CT Law, but the FTA may impose conditions through future administrative guidance.

Are loans agreed before corporate tax was introduced exempt from the interest cap?

Yes. Under Article 11 of Ministerial Decision No. 126 of 2023, net interest expenditure on debt instruments with terms agreed before 9 December 2022 is excluded from the GILDR and is fully deductible. This grandfathering only applies to the original loan terms. Refinanced or materially amended loans may lose this protection for the renegotiated portion.

Are banks and insurance companies subject to the GILDR in UAE?

No. Banks and insurance companies are exempt from the GILDR. In a UAE tax group that includes a bank or insurance member, that member’s interest income and expenditure is excluded from the group-level net interest expenditure and EBITDA calculation entirely under Article 12(5) of Ministerial Decision No. 126 of 2023.

What is adjusted EBITDA for UAE CT GILDR purposes?

For GILDR, adjusted EBITDA equals taxable income plus net interest expenditure plus depreciation and amortisation for the period, as set out in Article 9 of Ministerial Decision No. 126 of 2023. It cannot fall below AED 0. This is specifically a tax-adjusted figure, not the accounting EBITDA from your P&L, and must be calculated separately for the corporate tax return.

What is the penalty if UAE corporate tax interest deductions are calculated incorrectly?

Incorrect corporate tax returns that understate taxable income can attract administrative penalties under Cabinet Decision No. 75 of 2023, including a fixed penalty plus a percentage of underpaid tax. The FTA can also re-assess prior periods during an audit. Getting the GILDR calculation documented and correct before filing avoids penalties and reduces audit risk. See our guide to what triggers an FTA corporate tax audit for the full list of risk factors.

Need Help with Your UAE Corporate Tax Interest Deduction Calculation?

If your business carries significant bank borrowings, Islamic finance facilities, or finance leases, the GILDR may affect your corporate tax return for the period ending 31 December 2025, due by 30 September 2026. Qaspro Global’s tax consultants calculate your exact GILDR position, document historical liability exemptions, record carry-forward disallowed interest, and ensure your CT return correctly handles the deduction cap. Contact us today for a free consultation.