Can You Deduct Bad Debts from UAE Corporate Tax in 2026?

Every UAE business carries receivables that may never be collected. A customer goes silent for six months. A client enters liquidation. A trading partner disputes an invoice and refuses to pay. In a pre-corporate-tax world, the accounting write-off was the end of the story. Under the UAE’s 9% corporate tax regime, how you treat that uncollectable amount directly affects your tax bill.

Qaspro Global, a UAE-based tax and accounting consultancy, regularly advises businesses that claim deductions incorrectly because they confuse accounting provisions with tax-deductible write-offs. This guide breaks down the exact rules, the three conditions the FTA requires, and the costly mistake most businesses make with IFRS 9 expected credit loss provisions.

What Is a Bad Debt Under UAE Corporate Tax Law?

A bad debt is a receivable amount that a business has recognised as income but can no longer collect. Under Article 28 of Federal Decree-Law No. 47 of 2022, expenditure incurred wholly and exclusively for the purposes of a taxable person’s business is deductible, provided it is not capital in nature. A bad debt write-off falls under this rule because the original sale generated taxable revenue, and the uncollectable portion represents a genuine business loss.

The critical distinction that catches most businesses: the FTA differentiates between a general provision (an estimate of future losses across your entire receivables book) and a specific write-off (a confirmed loss on an identified debt). Only the specific write-off qualifies as a deductible expense.

Why Are General Provisions for Doubtful Debts NOT Deductible?

Under IFRS 9, businesses must recognise expected credit losses (ECL) on trade receivables from day one. This means your accounting records show a provision even for debts that are only 30 days overdue. The provision is an estimate of future losses based on probability-weighted scenarios, not a confirmed loss on a specific customer.

For UAE corporate tax purposes, this general ECL provision is not deductible. The FTA does not allow you to reduce taxable profit based on a statistical estimate of potential future losses. The provision sits on your balance sheet and reduces your accounting profit, but when calculating taxable income, you must add it back.

| Type | What It Is | CT Deductible? | Action Required |

|---|---|---|---|

| General provision (IFRS 9 ECL) | Estimate of future losses across all receivables | No | Add back when calculating taxable income |

| Specific provision | Provision against an identified customer debt | No (until written off) | Add back until formally written off |

| Specific write-off | Confirmed loss on an identified debt, removed from books | Yes (if 3 conditions met) | Deduct in the tax period of write-off |

| Recovered bad debt | Previously written-off amount collected | Taxable income | Include in taxable income in the period of recovery |

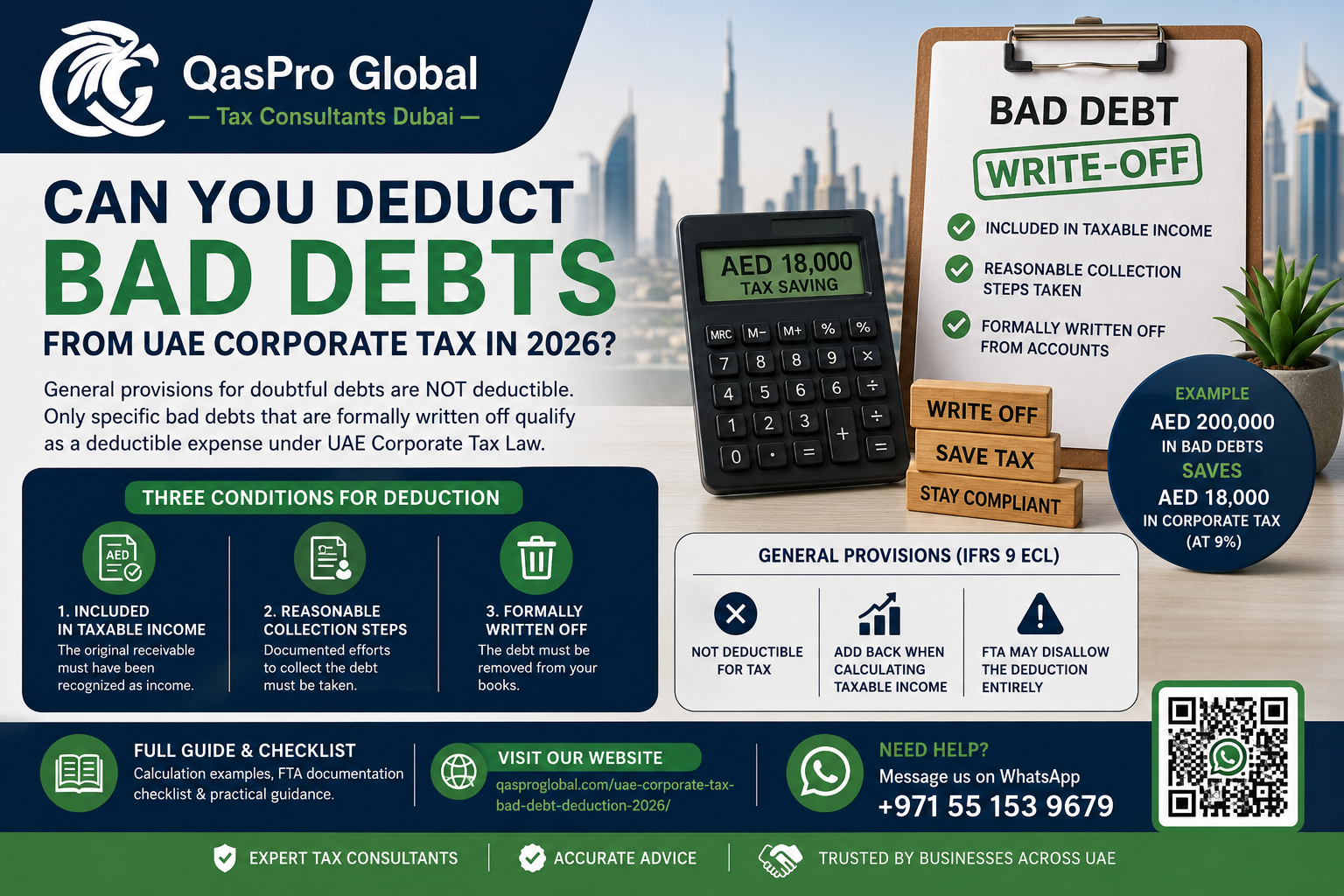

What Are the 3 Conditions for Deducting a Bad Debt?

A specific bad debt qualifies as a deductible expense for UAE corporate tax only when all three conditions are satisfied:

Condition 1: The Debt Was Included in Taxable Income

The original transaction that created the receivable must have been recognised as income in your financial statements. This means you used accrual-basis accounting and recorded the revenue when the invoice was issued, not when payment was received. If you use cash-basis accounting (available for businesses with revenue under AED 3 million under Ministerial Decision No. 114 of 2023), bad debt deductions do not apply because you never recognised the income in the first place.

Condition 2: Reasonable Steps to Collect Were Taken

You must demonstrate to the FTA that genuine efforts were made to recover the amount. The term “reasonable steps” is not explicitly defined in the law, but the FTA expects evidence of escalating collection efforts proportional to the debt size:

- Payment reminders: at least 2-3 documented reminder emails or letters

- Follow-up calls: logged telephone calls to the debtor

- Final demand: a formal demand letter with a deadline for payment

- Legal action: for debts above AED 50,000, engagement of a debt collection agency or filing a legal claim strengthens the deduction

- Debtor insolvency: evidence that the customer has entered liquidation, bankruptcy, or has absconded from the UAE

- UAE CT Interest Deduction Cap 2026: The AED 12M Rule

A business that simply writes off a receivable without any collection evidence risks the FTA disallowing the deduction during an audit.

Condition 3: The Debt Is Formally Written Off in Accounting Records

The debt must be removed from your accounts receivable and recorded as a bad debt expense in your income statement. A provision alone is not sufficient. The write-off must be:

- Approved by management (ideally documented in a Bad Debt Write-Off Approval Form)

- Recorded in the correct tax period

- Supported by the original invoice, contract, and collection correspondence

How Does a Bad Debt Write-Off Affect Your UAE Corporate Tax Bill?

Consider a trading company in Dubai with AED 5,000,000 in revenue and AED 3,800,000 in deductible expenses. During the 2025 tax period, it identifies AED 200,000 in receivables that are confirmed uncollectable.

| Scenario | Without Write-Off | With Write-Off |

|---|---|---|

| Revenue | AED 5,000,000 | AED 5,000,000 |

| Deductible expenses | AED 3,800,000 | AED 3,800,000 |

| Bad debt deduction | AED 0 | AED 200,000 |

| Taxable income (above AED 375,000) | AED 825,000 | AED 625,000 |

| Corporate tax at 9% | AED 74,250 | AED 56,250 |

| Tax saved | – | AED 18,000 |

That AED 200,000 write-off saves AED 18,000 in corporate tax. For businesses with larger receivables books, the savings multiply. A construction company with AED 1,000,000 in uncollectable receivables saves AED 90,000.

What Happens If a Written-Off Debt Is Later Recovered?

If a customer pays an amount that was previously written off and deducted from taxable income, the recovered amount must be included as taxable income in the tax period when the payment is received. This follows the standard accounting treatment: the reversal of a bad debt expense appears as income in the income statement, and for corporate tax purposes, it increases taxable profit.

Example: You wrote off AED 100,000 in 2025 and claimed the deduction. In 2026, the customer pays AED 60,000. That AED 60,000 is taxable income in your 2026 CT return. The remaining AED 40,000 stays as a deducted loss unless recovered later.

How Does IFRS 9 Expected Credit Loss Interact with Corporate Tax?

IFRS 9 requires businesses to recognise expected credit losses on trade receivables using a forward-looking model. This creates a timing difference between accounting profit and taxable income:

Stage 1: 12-Month ECL (Performing Receivables)

As soon as a receivable is recognised, IFRS 9 requires a provision based on 12-month expected credit losses. This provision reduces accounting profit but is not deductible for CT purposes. It must be added back when calculating taxable income.

Stage 2: Lifetime ECL (Significantly Deteriorated)

When credit risk increases significantly (e.g., customer misses a payment), the provision jumps to lifetime expected credit losses. This larger provision still reduces accounting profit but remains not deductible for CT purposes.

Stage 3: Credit-Impaired (Default)

When the receivable is credit-impaired (e.g., customer in liquidation), the provision equals the full expected loss. Even at this stage, the provision is not deductible until the debt is formally written off.

The tax deduction only occurs when the business moves from provision to write-off: removing the receivable from the balance sheet and recognising the confirmed loss in the income statement.

What Documentation Does the FTA Expect?

Qaspro Global advises all clients to maintain a Bad Debt Write-Off File for each deducted amount. This file should contain:

- Original invoice and contract proving the sale occurred

- Proof of income recognition showing the revenue was included in a prior CT return

- Collection correspondence with dates: reminders, demands, legal notices

- Evidence of uncollectibility: bounced cheques, customer liquidation notice, court judgment, or trade licence cancellation

- Management approval: a signed Bad Debt Write-Off Approval Form with the amount, customer name, invoice references, and reason for write-off

- Accounting entry: the journal entry debiting bad debt expense and crediting accounts receivable

The FTA can request this documentation during an audit. Without it, the entire deduction is disallowed and the tax plus a penalty applies.

How Does Bad Debt Relief Work for VAT?

Bad debt relief for VAT operates under separate rules from corporate tax. Under Article 64 of the VAT Executive Regulation, a VAT-registered business can recover the 5% output VAT it already paid to the FTA on an invoice that was never collected. All four conditions must be met:

| Condition | Requirement |

|---|---|

| Taxable supply | Output VAT was charged and reported on the VAT return |

| Time elapsed | At least 6 months have passed since the payment due date |

| Written off | The debt is written off in the business’s accounting records |

| Debtor notified | The debtor has been notified of the write-off |

The VAT bad debt adjustment is made in Box 7 of the VAT return (VAT Form 201). If the debtor later pays, the recovered VAT must be declared as output tax in the period of recovery.

Businesses should process the corporate tax bad debt write-off and the VAT bad debt relief simultaneously to maximise the tax benefit from uncollectable receivables.

What Are the Most Common Bad Debt Mistakes in UAE Corporate Tax?

Mistake 1: Deducting the IFRS 9 ECL Provision Instead of the Write-Off

Many businesses assume their accounting provision automatically reduces taxable income. It does not. The ECL provision must be added back. Only the confirmed write-off is deductible.

Mistake 2: Writing Off Without Collection Evidence

A write-off without documented collection efforts gives the FTA grounds to disallow the deduction. The result: taxable income increases by the full write-off amount, plus a potential penalty for incorrect filing.

Mistake 3: Timing the Write-Off in the Wrong Tax Period

A bad debt must be written off in the period when it becomes uncollectable, not in a future period chosen for tax planning convenience. The FTA can challenge write-offs that appear timed to reduce tax in a specific period.

Mistake 4: Forgetting to Include Recovered Debts in Income

When a previously written-off debt is recovered, businesses sometimes forget to reverse the deduction. This creates an understatement of taxable income that the FTA can identify during a reconciliation audit.

Mistake 5: Ignoring the VAT Bad Debt Relief

Businesses that write off a bad debt for CT purposes but forget to claim the VAT relief lose the 5% output tax as well. On a AED 500,000 uncollectable invoice, that is AED 25,000 in VAT that could have been recovered.

Can Businesses Using Small Business Relief Claim Bad Debt Deductions?

Businesses that elect Small Business Relief under Ministerial Decision No. 73 of 2023 are treated as having zero taxable income if their revenue does not exceed AED 3 million. Because taxable income is zero, bad debt deductions are irrelevant during the SBR period. However, Small Business Relief expires for tax periods ending after 31 December 2026, so businesses losing SBR eligibility from 2027 must begin tracking bad debts for CT purposes.

What About Related Party Bad Debts?

If the uncollectable debt is owed by a connected person under Article 36 of Federal Decree-Law No. 47 of 2022 (owners, directors, officers, relatives, or entities under common control), the FTA will scrutinise the write-off more closely. The arm’s length principle applies: the original transaction must have been at market value, and the write-off must reflect genuine commercial uncollectibility, not a disguised distribution or benefit to a related party.

Writing off a loan to a shareholder’s related company without exhausting all recovery options is a red flag that can trigger an FTA audit. Document the commercial substance thoroughly.

Frequently Asked Questions

Is a general provision for doubtful debts deductible under UAE corporate tax?

No. General provisions, including IFRS 9 expected credit loss provisions, are not deductible for UAE corporate tax purposes. Only specific bad debts that are formally written off in accounting records qualify for deduction under Article 28 of Federal Decree-Law No. 47 of 2022.

What are the conditions for deducting a bad debt from UAE corporate tax?

Three conditions must be met: the debt was previously included in taxable income under accrual accounting, reasonable steps were taken to collect the amount, and the debt is formally written off in the business’s accounting records with management approval.

How much tax does a bad debt write-off save?

A bad debt write-off saves 9% of the written-off amount. For example, writing off AED 200,000 in uncollectable receivables saves AED 18,000 in corporate tax. The savings only apply to amounts above the AED 375,000 zero-rate threshold.

Do I need to include recovered bad debts in taxable income?

Yes. If a previously written-off and deducted bad debt is later recovered, the recovered amount must be included as taxable income in the tax period when payment is received.

Can I claim VAT bad debt relief at the same time as a corporate tax deduction?

Yes. VAT bad debt relief and corporate tax bad debt deductions operate under separate rules. You should claim both simultaneously. VAT relief requires 6 months from the payment due date, a write-off in accounting records, and notification to the debtor.

What happens if the FTA disallows my bad debt deduction?

The disallowed amount is added back to taxable income, increasing your corporate tax liability. You may also face a penalty for filing an incorrect CT return. The administrative penalty for an incorrect return is AED 500 for the first occurrence and AED 1,000 for repeated violations within 24 months under Cabinet Decision No. 75 of 2023.

Does bad debt deduction apply to cash-basis businesses?

No. Cash-basis accounting (available for businesses with revenue under AED 3 million under Ministerial Decision No. 114 of 2023) recognises income when received, not when invoiced. Since the income was never recognised, there is no bad debt to deduct.

How long should I wait before writing off a debt?

There is no fixed timeframe in the law. However, most UAE businesses write off debts after 12 to 18 months of non-payment combined with exhausted collection efforts. For VAT bad debt relief, a minimum of 6 months from the payment due date is required. The key factor is demonstrating genuine uncollectibility, not the passage of time alone.

Need Expert Help?

Qaspro Global’s corporate tax consultants help UAE businesses correctly identify, document, and deduct bad debts to reduce their CT liability. From IFRS 9 ECL adjustments to FTA-ready write-off documentation, we ensure your deductions stand up to audit. Contact us today for a free consultation, or reach us on WhatsApp: +971 55 153 9679.

Related Reading

- UAE Corporate Tax Deductible Expenses 2026: Complete Guide (Article 28)

- UAE Corporate Tax Entertainment Expenses 2026: The 50% Rule

- 7 Corporate Tax Red Flags That Trigger an FTA Audit in UAE 2026

For a full breakdown of the legal requirements, see our guide on record retention requirements under UAE law.

General bad debt provisions are added back to profit when you work through the corporate tax calculation.

Writing off a debt is a realisation event, while a fair-value drop is not, a distinction explained in our guide to unrealised gains and the realisation basis.

If your Corporate Tax return contains an error, submitting a UAE corporate tax voluntary disclosure 2026 immediately is the most cost-effective way to avoid the 15% fixed FTA penalty.

Related Reading

- UAE Corporate Tax 2026: Don’t Pay 9% on Unrealised Gains

- How to Calculate UAE Corporate Tax 2026: 9 Profit Adjustments

- Got an FTA Audit Notice? The AED 20,000 Mistake Most UAE Businesses Make Next

- UAE Corporate Tax Deductible Expenses 2026: Complete Guide

- UAE CT 2026: Are You Using the Wrong Accounting Standard?

- UAE Small Business Relief Expires December 31

- UAE Corporate Tax Loss Carry Forward 2026

- UAE Corporate Tax Interest Deduction Cap 2026

- UAE Corporate Tax Entertainment Expenses 2026

- UAE Corporate Tax Penalties 2026: Every FTA Fine Explained

- How to Pay UAE Corporate Tax 2026: GIBAN Steps

- UAE Tax Deadlines 2026: Every Date Your Business Must Know

Founder & CEO, Qaspro Global — UAE tax expert with 16+ years of experience in VAT, corporate tax and FTA audit support.