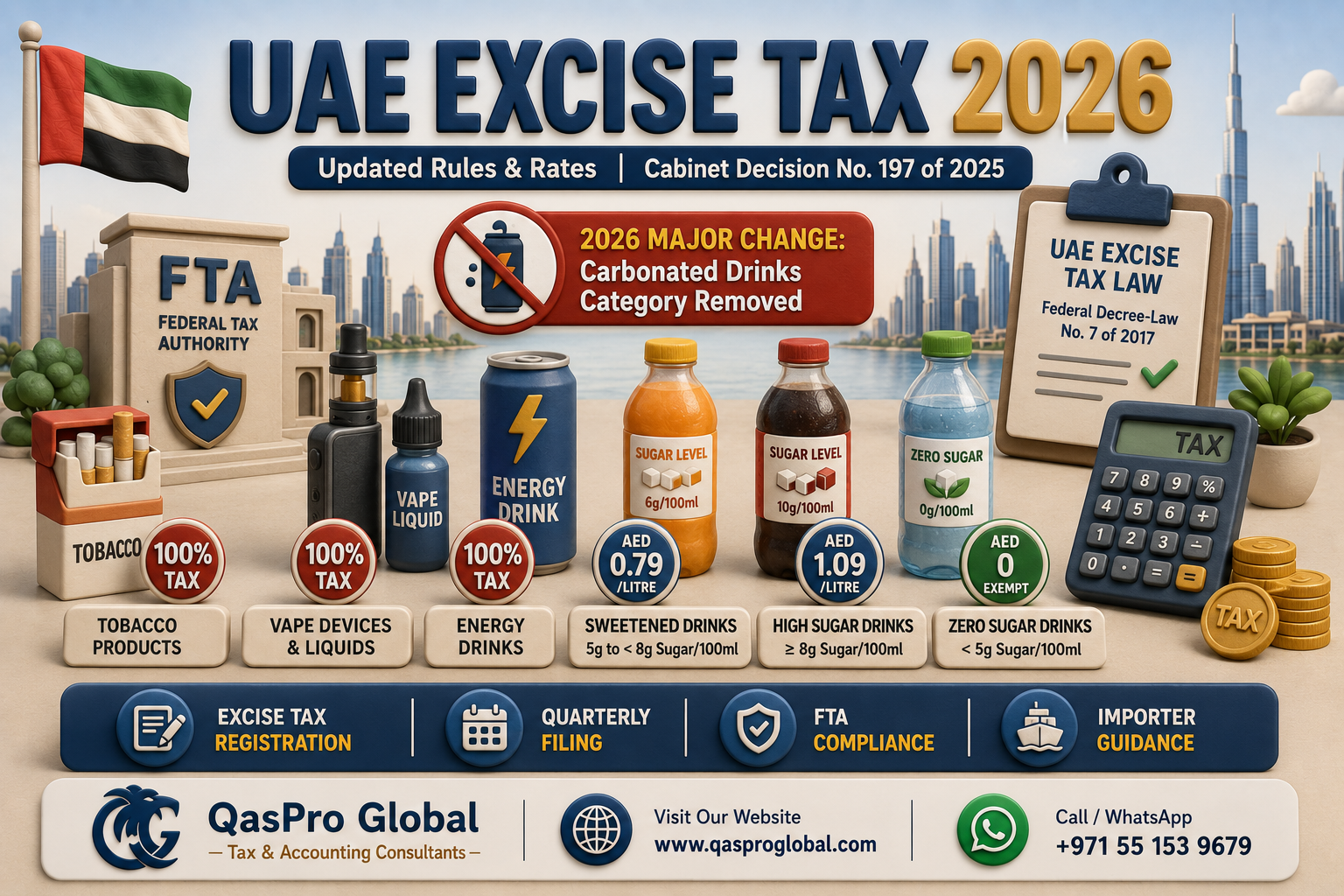

What Is UAE Excise Tax and Which Products Does It Cover in 2026?

UAE excise tax is a federal tax on goods deemed harmful to health under Federal Decree-Law No. 7 of 2017. The Federal Tax Authority administers it, and any business that imports, produces, or stores excise goods in the UAE must register before its first taxable activity. Cabinet Decision No. 197 of 2025, effective 1 January 2026, updated the complete list of excise goods and introduced a significant change to how sweetened drinks are taxed, removing the old flat-rate carbonated drinks category entirely.

In this guide, Qaspro Global, a UAE-based tax and accounting consultancy, breaks down every excise good, the current 2026 rates, who must register, how filing works, and the key changes that came into force at the start of this year.

Quick Answer: What Are the UAE Excise Tax Rates in 2026?

Five categories of goods are subject to UAE excise tax. Tobacco products, electronic smoking devices, vape liquids, and energy drinks are all taxed at 100% of the excise price. Sweetened drinks are now taxed on a tiered sugar-content basis: AED 0 per litre for drinks with less than 5 grams of sugar per 100ml, AED 0.79 per litre for drinks with 5 to less than 8 grams, and AED 1.09 per litre for drinks with 8 grams or more per 100ml. Carbonated drinks are no longer a separate excise category as of 1 January 2026.

Full UAE Excise Tax Rates Table 2026

The rates below are taken directly from Article 10 of Cabinet Decision No. 197 of 2025 and apply from 1 January 2026:

| Excise Good | Tax Rate or Amount | Legal Basis |

|---|---|---|

| Tobacco and tobacco products | 100% of excise price | Art. 10(1), CD 197/2025 |

| Liquids used in electronic smoking devices (vape liquids, whether nicotine-free or not) | 100% of excise price | Art. 10(2), CD 197/2025 |

| Electronic smoking devices and tools (vapes, e-hookahs, heated tobacco devices) | 100% of excise price | Art. 10(3), CD 197/2025 |

| Energy drinks | 100% of excise price | Art. 10(4), CD 197/2025 |

| Sweetened drinks: 5g to less than 8g sugar per 100ml | AED 0.79 per litre | Art. 10(5), CD 197/2025 |

| Sweetened drinks: 8g or more sugar per 100ml | AED 1.09 per litre | Art. 10(6), CD 197/2025 |

| Sweetened drinks: less than 5g sugar per 100ml | AED 0 (exempt) | Art. 10(7), CD 197/2025 |

| Sweetened drinks with only artificial sweeteners (less than 5g added sugar) | AED 0 (exempt) | Art. 10(8), CD 197/2025 |

The key 2026 change: Under Cabinet Decision No. 52 of 2019, all carbonated drinks were taxed at a flat 50% rate regardless of sugar content. From 1 January 2026, carbonated drinks are no longer a standalone excise category. Plain sparkling water with no added sugar is now fully exempt. A sweetened carbonated drink is assessed under the tiered sweetened drinks rules based on its actual sugar content per 100ml.

What Counts as a Tobacco Product Under UAE Excise Tax?

Tobacco and tobacco products cover all goods listed in Chapter 24 of the GCC Common Customs Tariff that are imported, cultivated, or produced in the UAE. This includes cigarettes, cigars, shisha tobacco, roll-your-own tobacco, pipe tobacco, and electrically heated cigarettes such as IQOS sticks. Under Article 3 of Cabinet Decision No. 197 of 2025, products exclusively intended to assist in smoking cessation and designated by the Minister of Finance are excluded from this category.

Practical example: A carton of 200 cigarettes with a retail price of AED 140 carries excise tax of AED 70 (100% applied to the excise price, which equals half the retail price at a 100% rate). VAT at 5% then applies on top of the AED 140 retail base, adding AED 7.

What Counts as an Electronic Smoking Device?

Electronic smoking devices include e-cigarettes, vaping devices, electronic hookahs (e-shisha), and electrically heated tobacco devices, whether or not they contain nicotine or tobacco. The applicable customs codes are set out in Ministerial Decision No. 1 of 2025 and cover four main HS code categories: reusable e-cigarettes (8543 40 10), electronic water pipes (8543 40 20), electrically heated cigarette devices (8543 40 30), and other electronic smoking tools (8543 40 90).

Vape liquids are taxed separately as a distinct excise category. A business importing both a vape device and a bottle of vape liquid pays 100% excise on each item independently.

What Are Energy Drinks Under UAE Excise Tax?

Energy drinks are any beverages marketed or sold as providing mental or physical stimulation through caffeine, taurine, ginseng, guarana, or substances with equivalent effects. Concentrates, powders, gels, and extracts that can be mixed into an energy drink are also subject to excise at 100% under Article 6 of Cabinet Decision No. 197 of 2025. The classification depends on how the product is marketed, not solely on its ingredient list. A drink branded as an energy supplement and containing stimulant substances qualifies even if it does not use the words “energy drink” on the label.

How the New Sweetened Drinks Rules Work in 2026

A sweetened drink is any product to which sugar, artificial sweeteners, or other sweeteners have been added, in ready-to-drink, concentrate, powder, gel, or extract form. The tax rate depends on the total sugar and sweetener content per 100ml of the final ready-to-drink beverage.

The following beverages are exempt from the sweetened drinks category regardless of sugar content:

- Beverages containing at least 75% milk of the ready-to-drink product

- Beverages containing at least 75% milk substitutes (oat, almond, soy drinks)

- Baby formula, follow-up formula, and baby food

- Beverages for special dietary needs under GCC Standard 654

- Beverages for medical use under GCC Standard 1366

- Sweetened drinks prepared in restaurants or similar establishments and served in open, unsealed containers for direct consumption by the end consumer

- Drinks containing alcohol

Worked examples:

- A 330ml can of cola with 10.6g sugar per 100ml: AED 1.09 x 0.33 = AED 0.36 excise per can

- A 500ml bottle of a moderately sweet fruit drink with 6g sugar per 100ml: AED 0.79 x 0.5 = AED 0.40 excise per bottle

- A 330ml can of zero-sugar diet soda with only artificial sweeteners: AED 0 excise

- A 500ml bottle of plain sparkling water with no added sugar: AED 0 excise

Who Must Register for UAE Excise Tax?

Excise tax registration is mandatory for any business that:

- Imports excise goods into the UAE (including through free zone ports)

- Produces or manufactures excise goods within the UAE

- Operates as a Warehouse Keeper in a Designated Zone holding excise goods

- Releases excise goods from a Designated Zone into UAE domestic consumption

- Stockpiles excise goods on which tax has not yet been paid

There is no turnover threshold for excise tax registration. Unlike VAT (AED 375,000 mandatory threshold) and corporate tax (AED 1 million for natural persons), any business that carries out even a single import of excise goods must register before that first activity. Registration is completed through the FTA EmaraTax portal at eservices.tax.gov.ae.

How Does UAE Excise Tax Filing Work?

Excise tax returns are filed quarterly through EmaraTax. The return and payment are due 15 days after the end of each quarter, which is stricter than the 28-day VAT deadline. Importers typically pay excise at the point of customs clearance before goods are released. The quarterly return reconciles all excise activity for the period including:

- Quantity and value of excise goods imported or produced

- Excise goods released from Designated Zones

- Deductible excise tax (on exported goods or returns)

- Net excise tax payable to the FTA

How VAT and Excise Tax Interact

VAT at 5% is charged on top of the excise tax. The VAT base for an excise good is the full excise price including the excise tax amount. For a tobacco product with an excise price of AED 10, the excise tax is AED 10 (100%). The total becomes AED 20, and VAT of 5% on AED 20 adds AED 1. The shelf price includes both taxes. Businesses selling excise goods must reflect both tax components correctly in their VAT returns and excise returns filed separately on EmaraTax.

UAE Excise Tax Penalties for Non-Compliance in 2026

The FTA imposes administrative penalties under Federal Decree-Law No. 28 of 2022 on Tax Procedures for excise tax violations:

- Failure to register before first taxable activity: AED 20,000 penalty

- Late filing of excise return: AED 1,000 for first occurrence, AED 2,000 for repeat violations within 24 months

- Late payment of excise tax due: 2% immediate surcharge plus escalating monthly penalties under Cabinet Decision No. 129 of 2025

- Failure to keep proper records: up to AED 20,000

- Physical inspection: Under Federal Decree-Law No. 17 of 2025, FTA inspectors can inspect excise goods warehouses and Designated Zones without prior notice

Customs authorities can also seize excise goods at the point of import if excise registration is not in place and tax is not paid prior to clearance.

Frequently Asked Questions

Is plain sparkling water subject to UAE excise tax in 2026?

No. Plain sparkling or carbonated water with no added sugar or sweeteners is not subject to excise tax from 1 January 2026. Under Cabinet Decision No. 197 of 2025, carbonated drinks are no longer a standalone excise category. Plain sparkling water does not fall under the sweetened drinks definition and carries zero excise.

Is Diet Coke or zero-sugar soda subject to UAE excise tax in 2026?

Sweetened drinks containing only artificial sweeteners with less than 5 grams of sugar per 100ml are exempt under Article 10(8) of Cabinet Decision No. 197 of 2025. A genuine diet or zero-sugar soda that meets this definition carries AED 0 excise from 1 January 2026. The product must still have no added sugar, not just no added cane sugar.

What is the excise tax rate on cigarettes in UAE 2026?

Tobacco and tobacco products are taxed at 100% of the excise price under Article 10(1) of Cabinet Decision No. 197 of 2025. For a pack retailing at AED 28, the excise price is AED 14 (the retail price divided by 2, since the tax equals 100% of the excise price which is half the retail inclusive price). The excise component embedded in the shelf price is AED 14.

Are vape liquids and vape devices taxed the same way?

Both are taxed at 100% of the excise price, but they are separate categories. The liquids (whether nicotine-containing or nicotine-free) are taxed under Article 10(2) of Cabinet Decision No. 197 of 2025. The devices themselves (e-cigarettes, e-hookahs, heated tobacco devices) are taxed separately under Article 10(3). A business importing a device with a pre-filled liquid cartridge pays excise on both the device value and the liquid value.

Do restaurants need to register for excise tax in the UAE?

A restaurant that buys excise goods (energy drinks, tobacco, soft drinks) from a UAE distributor that has already paid excise does not need to register. Excise is paid once at the import or production stage. However, sweetened drinks served in open, unsealed containers directly to customers on the premises are exempt from excise entirely under Article 7(5)(f) of Cabinet Decision No. 197 of 2025, so the restaurant effectively bears no excise cost on those items.

How is excise tax calculated on sweetened drink concentrate?

For concentrates, powders, and gels that produce a sweetened drink when mixed, the sugar content is calculated based on the final ready-to-drink product as per the producer’s mixing guidelines. If guidelines are unavailable, the FTA determines the calculation method. The tax rate per litre then applies to the equivalent volume of finished drink that each unit of concentrate produces.

Is excise tax deductible under UAE corporate tax?

Excise tax paid as part of the cost of acquiring goods used in business operations is generally deductible as a business expense under Article 28 of Federal Decree-Law No. 47 of 2022. Excise tax collected from customers and remitted to the FTA is not a business expense, as it is a tax liability being passed through. The deductibility treatment is similar to how input VAT that is not recoverable can be treated as a cost.

What happened to the 50% carbonated drinks excise rate?

The flat 50% excise rate on carbonated drinks, which applied under Cabinet Decision No. 52 of 2019, was removed from 1 January 2026. Cabinet Decision No. 197 of 2025 replaced it with the tiered sweetened drinks approach based on sugar content. A sweetened carbonated drink is now taxed at AED 0.79 or AED 1.09 per litre depending on its sugar level. A plain carbonated drink with no added sugar pays zero excise. Businesses that were accounting for the 50% rate should have updated their cost models at the start of 2026.

Can excise goods be stored in UAE free zones without paying excise tax?

Yes. Excise goods stored in FTA-licensed Designated Zones are held in tax suspension. A licensed Warehouse Keeper manages the goods and excise tax is not due until the goods are released into UAE domestic consumption. Direct export of excise goods from a Designated Zone out of the UAE is also exempt from excise under Article 4 of Federal Decree-Law No. 7 of 2017. This is similar to the VAT treatment of Designated Zones.

When did UAE excise tax start and what has changed since?

UAE excise tax launched on 1 October 2017 covering tobacco and energy drinks at 100%. Carbonated drinks at 50% and sweetened drinks were added from 1 December 2019 under Cabinet Decision No. 52 of 2019. Electronic smoking devices and vape liquids were included in the same 2019 expansion. The latest update, Cabinet Decision No. 197 of 2025 effective 1 January 2026, removed the separate carbonated drinks category and replaced it with a sugar-content tiered approach for all sweetened drinks, reducing the tax on low-sugar and diet beverages to zero.

Need Help with Excise Tax Registration or FTA Compliance?

Qaspro Global’s tax compliance team handles excise tax registration, quarterly return filing, and FTA correspondence for businesses importing or producing tobacco, beverages, or electronic smoking products in the UAE. If your product category was affected by the January 2026 rule changes, or if you are a new importer of excise goods who needs to register before your next shipment, contact us today for a free consultation.

Related Reading

- UAE VAT Return Filing 2026: Deadlines, Steps and How to Avoid Fines

- UAE Tax Deadlines 2026: Every Date Your Business Must Know

- Got an FTA Penalty? The 40-Day Reconsideration Window UAE 2026

- UAE E-Invoicing 2026: Miss This and Pay AED 5,000 Every Month

Founder & CEO, Qaspro Global — UAE tax expert with 16+ years of experience in VAT, corporate tax and FTA audit support.