UAE Corporate Tax Interest Deduction: What Changed for 2026?

One financing mistake can turn a normal loan interest expense into a non-deductible Corporate Tax adjustment. The UAE Corporate Tax interest deduction rules are now a real filing issue for companies using bank loans, shareholder loans, intercompany funding, Islamic finance, group treasury arrangements or director financing.

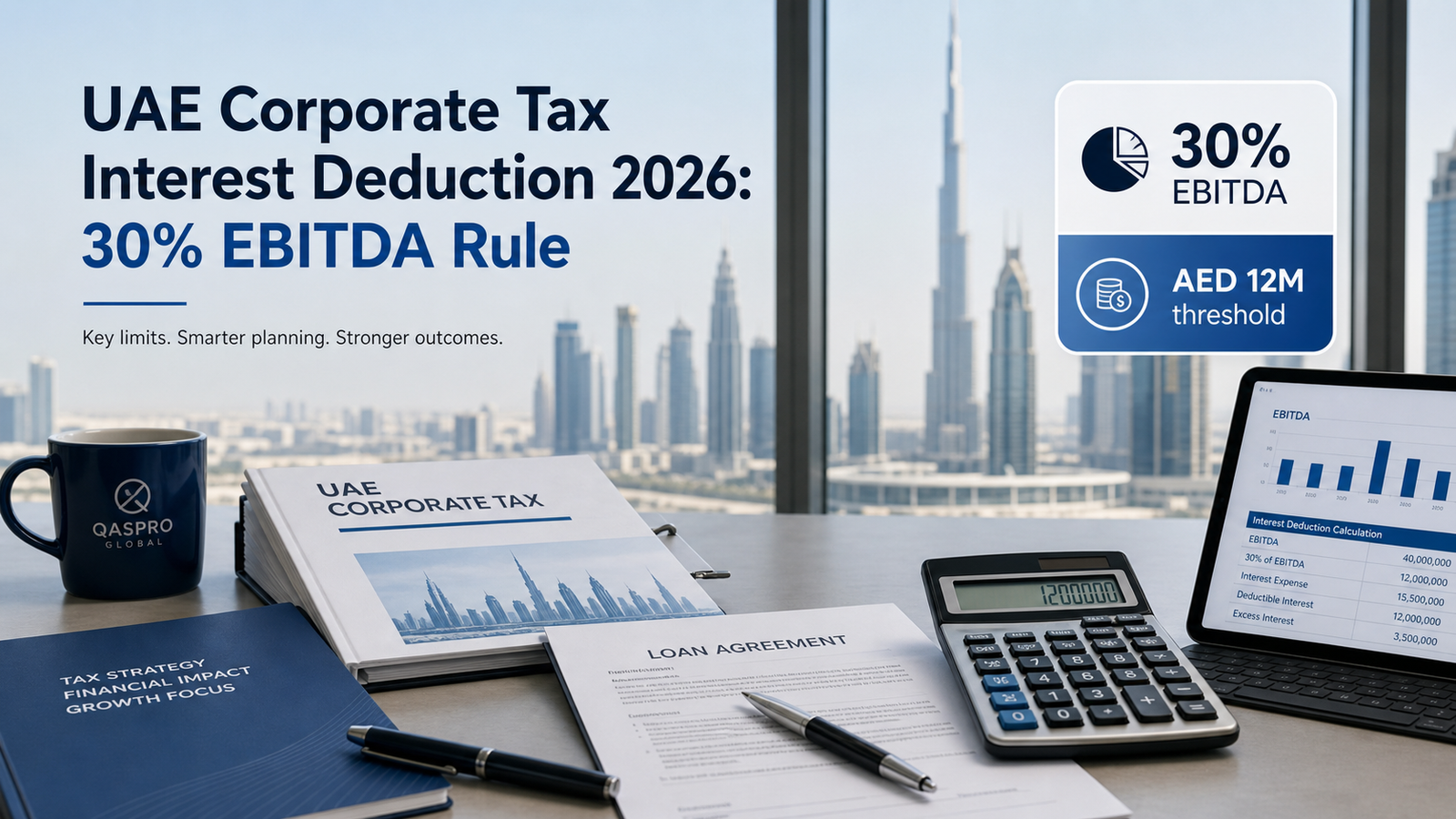

This 2026 guide explains the 30% EBITDA rule, the AED 12 million net interest threshold, related-party loan risk, documentation, filing treatment and practical examples for UAE companies. Qaspro Global, a UAE-based tax and accounting consultancy, prepared this guide for business owners, finance managers and CFOs preparing Corporate Tax filings.

Why Interest Deduction Matters Now

Many UAE companies were used to treating finance costs as a normal accounting expense. Corporate Tax changes that approach. The starting point for taxable income is accounting income, but the law then requires adjustments for non-deductible or limited expenditure. Interest is one of the most important adjustments because debt can move profit between related parties, reduce taxable income or create artificial financing costs if it is not properly supported.

The risk is highest for owner-managed companies, free zone groups, real estate companies, holding companies, trading businesses with shareholder loans and groups with central treasury funding. If the file does not show why the loan exists, how the rate was set and how the proceeds were used, the deduction can be challenged.

UAE Corporate Tax Interest Deduction Rules at a Glance

| Rule | What it means | Practical action |

|---|---|---|

| Article 28 business purpose test | Expenditure must be incurred wholly and exclusively for business purposes, subject to other limitations. | Keep contracts, board approvals, bank evidence and business purpose notes. |

| Article 30 general limitation | Net interest expenditure may be limited to 30% of accounting EBITDA unless exclusions or threshold rules apply. | Calculate net interest, accounting EBITDA and disallowed carry-forward. |

| AED 12 million threshold | The Ministerial Decision sets a de minimis threshold for net interest expenditure. | If net interest is below the threshold, document the calculation anyway. |

| Article 31 specific limitation | Certain related-party financing linked to exempt income, qualifying group transfers or business restructuring relief can be restricted unless the main purpose is not a Corporate Tax advantage. | Review shareholder loans, acquisition loans, dividend funding and group restructuring finance. |

| Article 34 transfer pricing | Related-party arrangements must meet the arm’s length standard. | Benchmark the rate and keep related-party disclosure support. |

How Does the 30% EBITDA Rule Work?

The 30% EBITDA rule limits net interest expenditure by reference to accounting EBITDA. In simple terms, the business starts with accounting earnings before interest, tax, depreciation and amortisation, then applies the Corporate Tax rules to calculate how much net interest can be deducted in the period. Interest above the allowed amount may be carried forward subject to the law and implementing decisions.

Example: if a UAE company has accounting EBITDA of AED 2,000,000, the 30% reference amount is AED 600,000. If its net interest expenditure is AED 850,000 and no exclusion applies, AED 250,000 may need to be carried forward rather than deducted immediately. The exact calculation must follow the law, Ministerial Decisions and FTA guidance, but the accounting file should already show the numbers clearly.

What Counts as Interest for UAE Corporate Tax?

The Corporate Tax Law defines interest broadly. It includes amounts accrued or paid for the use of money or credit, discounts, premiums, Islamic finance profit and other amounts economically equivalent to interest. This means the review is not limited to a line called bank interest. A tax reviewer should inspect finance charges, factoring, shareholder loan profit, intercompany mark-ups, late payment finance costs and Islamic facility profit.

Do not rely only on the chart of accounts label. If a payment is economically connected to financing, it should be tested. Qaspro Global normally reconciles the trial balance to loan schedules, bank statements, finance agreements and related-party accounts before finalising the deduction.

When Does the AED 12 Million Threshold Help?

The UAE Ministerial Decision on the general interest deduction limitation rule sets an AED 12 million threshold for net interest expenditure. For many small and mid-sized UAE companies, this means the full 30% EBITDA calculation may not create a practical disallowance if net interest expenditure is below the threshold. However, this is not a reason to ignore documentation.

The threshold does not remove the business purpose test, related-party arm’s length requirement or specific interest limitation rules. A shareholder loan with a weak commercial reason can still be challenged even where the net interest amount is below AED 12 million. Keep the calculation and the loan support together in the Corporate Tax working paper.

Related-Party Loans: The Biggest Audit Risk

Article 34 requires related-party transactions and arrangements to meet the arm’s length standard. A loan from a shareholder, director, sister company, parent company or group treasury company is not automatically wrong. The problem starts when the rate, term, currency, repayment schedule, security and commercial purpose do not match what independent parties would have agreed.

| Loan feature | Risk question | Evidence to keep |

|---|---|---|

| Interest rate | Is the rate commercially supportable? | Bank quotes, benchmark data, facility comparison, credit profile. |

| Loan purpose | Was the borrowing used for business activity? | Board note, supplier payments, asset purchase records, working capital schedule. |

| Repayment terms | Would an independent lender accept the term? | Loan agreement, repayment calendar, covenant notes. |

| Connected persons | Is the lender an owner, director or related party? | Ownership chart, related-party disclosure, transfer pricing file. |

Specific Interest Limitation: When a Loan Is Not Just a Loan

Article 31 restricts deductions for interest expenditure incurred on a loan obtained directly or indirectly from a related party in certain cases, unless the taxable person can demonstrate that the main purpose of obtaining the loan and carrying out the relevant transaction is not to gain a Corporate Tax advantage. The risk areas include dividends, capital contributions, share acquisitions, ownership interest acquisitions and transactions linked to exempt income or reliefs.

If a group borrows from a related party to fund a dividend, acquire a related company, contribute capital or move assets under relief provisions, the tax file needs more than an invoice. It needs a commercial explanation, board approval, funding trail and tax position paper.

Step-by-Step Interest Deduction Checklist for 2026 Filing

- Extract all finance cost accounts from the trial balance.

- Separate bank interest, Islamic finance profit, shareholder loan interest, intercompany interest and other financing costs.

- Calculate interest income and net interest expenditure.

- Check whether the AED 12 million threshold applies.

- Calculate accounting EBITDA and the 30% reference amount where needed.

- Review Article 31 specific limitation for related-party financing.

- Benchmark related-party loan rates under Article 34.

- Prepare the related-party disclosure support and transfer pricing file where required.

- Document any carried-forward disallowed interest.

- Keep loan agreements, bank statements and board approvals with the Corporate Tax return file.

Official Sources Used

Official sources: Ministry of Finance Corporate Tax page, Federal Decree-Law No. 47 of 2022 and amendments, Article 28, Article 30, Article 31, Article 34 and Article 55. The Ministry of Finance states that UAE Corporate Tax applies from financial years beginning on or after 1 June 2023 and that taxable persons file returns within 9 months from the end of the relevant tax period.

Source links: Ministry of Finance Corporate Tax page and Corporate Tax Law PDF.

Frequently Asked Questions

What is the UAE Corporate Tax 30% EBITDA interest rule?

It is the general interest deduction limitation rule under Article 30. It can limit deductible net interest expenditure to 30% of accounting EBITDA, subject to Ministerial Decision rules, exclusions and threshold treatment.

Is all bank interest deductible in UAE Corporate Tax?

No. Bank interest still needs to satisfy the business purpose test and the general interest limitation rule where applicable. The accounting deduction and tax deduction are not always identical.

Does the AED 12 million threshold mean no review is needed?

No. The threshold can reduce practical exposure for smaller businesses, but it does not remove Article 28, Article 31 or Article 34 documentation requirements.

Are shareholder loans allowed?

Yes, but the rate, term and business purpose must be supportable. Related-party shareholder loans should be benchmarked and documented under the arm’s length principle.

Can disallowed interest be carried forward?

Interest that is disallowed under the general limitation may be carried forward subject to the law and implementing decisions. Track it separately in the Corporate Tax working paper.

Do free zone companies need to apply these rules?

Yes. Free zone companies within the Corporate Tax regime should review interest deductions, especially where they claim 0% treatment as a Qualifying Free Zone Person.

What documents should support interest deduction?

Keep loan agreements, bank statements, payment schedules, board approvals, related-party disclosures, transfer pricing support, use-of-funds evidence and the EBITDA calculation.

Can Qaspro Global review my loan interest before filing?

Yes. Qaspro Global can review loan agreements, related-party balances, EBITDA calculations and Corporate Tax return treatment before filing.

Need Help Before Your Corporate Tax Filing?

Qaspro Global can prepare your Corporate Tax interest deduction schedule, related-party loan support, transfer pricing working papers and filing checklist. Read also our UAE transfer pricing guide, Corporate Tax filing deadline guide, depreciation rules guide and QFZP qualifying income guide. For employment visa and MOHRE documentation support, see Yalah Dubai’s guide to UAE work permit categories 2026.

Founder & CEO, Qaspro Global — UAE tax expert with 16+ years of experience in VAT, corporate tax and FTA audit support.