What Happens When the FTA Sends You an Audit Notice in the UAE?

Quick Answer: The Federal Tax Authority must give you at least 10 business days’ notice before a tax audit under Article 16 of Federal Decree-Law 28 of 2022. Refusing to cooperate triggers a fixed AED 20,000 penalty under Cabinet Decision 75 of 2023. If the FTA finds errors you did not voluntarily disclose, you face a 15% fixed penalty plus 1% per month on the tax difference. A registered tax agent can represent you, negotiate with auditors, and often reduce the final assessment significantly.

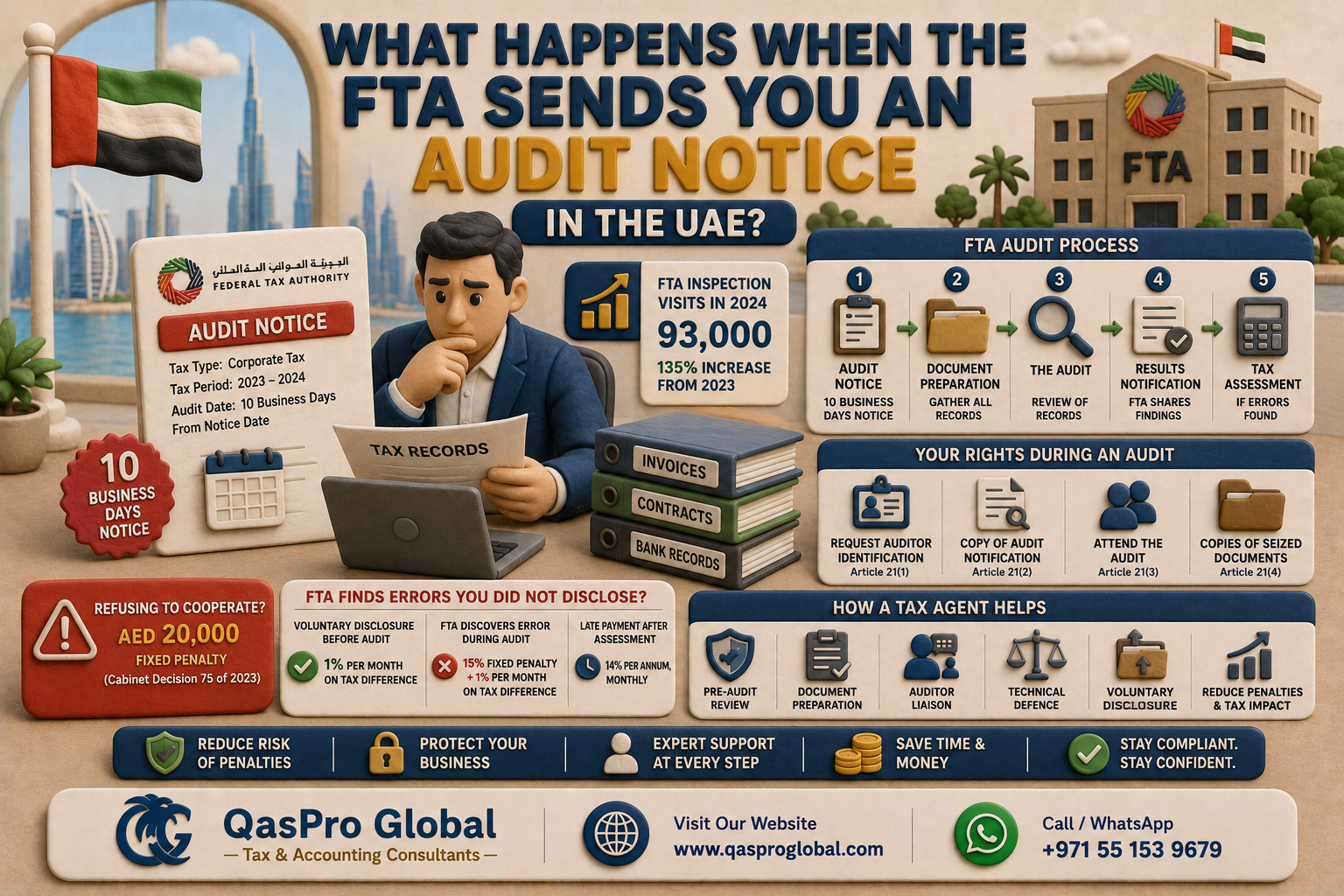

The FTA conducted 93,000 inspection visits in 2024, a 135% increase compared to the year before. With corporate tax now fully in force and the first CT filing deadline of September 30, 2026 approaching, audit activity is expected to accelerate further. If you receive an FTA audit notice, the next steps you take determine whether the outcome is a clean bill or a six-figure penalty assessment. Qaspro Global, a UAE-based tax and accounting consultancy, has prepared this guide so you know exactly what to expect, what your rights are, and when professional FTA audit support makes financial sense.

What Is an FTA Tax Audit in the UAE?

An FTA tax audit is a formal procedure where the Federal Tax Authority inspects your commercial records, information, data, and goods to verify whether you have met all tax obligations under Federal Decree-Law 28 of 2022 (Tax Procedures Law) and the relevant tax law. The audit may cover VAT, corporate tax, or excise tax, and it can examine any tax period within the past five years.

Tax audits differ from the routine compliance checks the FTA runs automatically through EmaraTax. An audit involves a dedicated Tax Auditor who reviews source documents, bank statements, invoices, contracts, and accounting records in detail. The auditor has the legal authority under Article 17 of the Tax Procedures Law to take original records, copies, and even product samples from your premises.

How Does the FTA Audit Process Work Step by Step?

The FTA audit follows a structured legal process defined in Articles 16 through 22 of Federal Decree-Law 28 of 2022. Understanding each step helps you prepare properly and avoid penalties.

Step 1: The Audit Notice (10 Business Days’ Warning)

The FTA sends a written notification at least 10 business days before the audit date (Article 16, Clause 2). The notice specifies the tax type, periods under review, and the location where the audit will take place. This is your preparation window.

Step 2: Document Preparation

Gather all records the FTA may request: tax returns, supporting schedules, invoices, bank statements, contracts, payroll records, transfer pricing documentation (if applicable), and your chart of accounts. All records must be available in Arabic or with certified Arabic translations (Article 5, FDL 28/2022).

Step 3: The Audit Itself

The Tax Auditor may conduct the audit at FTA premises, your place of business, or any location where you store records (Article 16, Clause 3). Audits take place during FTA working hours unless the Director General authorises an exception (Article 18).

Step 4: Audit Results Notification

After the audit, the FTA informs you of the results within the timeframe specified in the Executive Regulation (Article 22). You have the right to view or obtain the documents on which the FTA based its assessment.

Step 5: Tax Assessment (If Errors Found)

If the audit reveals unpaid tax, the FTA issues a Tax Assessment under Article 23, notifying you within 10 business days. The assessment may include additional tax owed plus administrative penalties.

When Can the FTA Enter Your Premises Without Notice?

The FTA can bypass the 10-day notice requirement and enter your business, storage, or record-keeping location without warning in three specific situations under Article 16, Clause 4 of the Tax Procedures Law:

- Suspected tax evasion: The FTA has serious grounds to believe you or another person is participating in tax evasion

- Obstruction risk: The FTA believes that not closing the premises would hinder the audit

- Access refusal: You were given the standard 10-day notice but attempted to stop the Tax Auditor from entering

In all three cases, the Tax Auditor must obtain prior written consent from the FTA Director General. If the premises is a residence, a Public Prosecution permit is also required. The FTA can temporarily close the premises for up to 72 hours, extendable with a Public Prosecution permit (Article 16, Clauses 5 and 6).

What Are Your Legal Rights During an FTA Audit?

Article 21 of Federal Decree-Law 28 of 2022 gives every person subject to a tax audit four specific legal rights. Knowing these rights prevents auditors from overstepping and protects your interests.

| Right | Legal Basis | What It Means in Practice |

|---|---|---|

| Request auditor identification | Article 21(1) | Ask the Tax Auditor to show their FTA job ID card before allowing access |

| Copy of audit notification | Article 21(2) | Obtain a copy of the official audit notice for your records |

| Attend the audit | Article 21(3) | You or your tax agent can be present during every audit activity outside FTA premises |

| Obtain copies of seized documents | Article 21(4) | Get copies of any original paper or digital documents the FTA takes during the audit |

Qaspro Global advises businesses to exercise all four rights from the first interaction. Request the auditor’s ID, keep a log of every document handed over, and ensure your tax agent is present at all times.

What Penalties Apply if You Do Not Cooperate with the FTA Audit?

Non-cooperation during an FTA tax audit is one of the most expensive mistakes a UAE business can make. Cabinet Decision 75 of 2023 (Clause 12) imposes a fixed penalty of AED 20,000 for failure to cooperate with or facilitate the Tax Auditor, as required under Article 20 of the Tax Procedures Law. This penalty applies to the business, its tax agent, or its legal representative, from their own funds.

But the AED 20,000 is only the beginning. The real financial damage comes from errors the FTA discovers that you did not voluntarily disclose:

| Scenario | Penalty (CD 75/2023) | Example on AED 500,000 Tax Difference |

|---|---|---|

| You file a voluntary disclosure BEFORE audit notice | 1% per month on tax difference (no fixed penalty) | AED 5,000/month |

| FTA discovers error during audit (Clause 11) | 15% fixed + 1% per month on tax difference | AED 75,000 fixed + AED 5,000/month |

| Non-cooperation with auditor (Clause 12) | AED 20,000 fixed | AED 20,000 (on top of other penalties) |

| Late payment after Tax Assessment (Clause 8) | 14% per annum, monthly | ~AED 5,833/month on AED 500K |

The difference between voluntary disclosure and FTA discovery is dramatic. On a AED 500,000 tax difference, voluntarily disclosing before the audit notice saves you at least AED 75,000 in the fixed 15% penalty alone. This is why professional tax support before and during the audit matters.

What Does a Tax Agent Do During an FTA Audit?

A registered tax agent is a professional listed in the FTA’s Tax Agent Register under Article 12 of the Tax Procedures Law. Only registered agents can formally represent you before the FTA. Here is what a tax agent handles during an audit:

- Pre-audit review: Examines your tax returns, supporting schedules, and records before the auditor arrives to identify and fix errors proactively

- Document preparation: Organises all records the FTA will request, ensuring nothing is missing (missing records trigger the AED 10,000/20,000 penalty under Clause 1 of CD 75/2023)

- Auditor liaison: Communicates directly with the Tax Auditor, answers technical questions, and provides clarifications on your behalf

- On-site attendance: Attends the audit at your premises under Article 21(3), ensuring your rights are respected and auditor requests are properly documented

- Technical defence: Challenges incorrect FTA positions with law references, FTA public clarifications, and supporting case precedent

- Voluntary disclosure filing: If errors are found during the pre-audit review, files a voluntary disclosure before the audit begins (saving you the 15% fixed penalty)

- Post-audit response: Reviews the Tax Assessment, prepares review requests (Article 28) or reconsideration requests (Article 29), and represents you before the Tax Disputes Resolution Committee if needed

How Much Does FTA Audit Support Cost in the UAE?

FTA audit support costs vary based on company size, audit complexity, tax type (VAT vs corporate tax vs both), number of tax periods under review, and the volume of transactions. Here is a realistic cost breakdown for 2026 based on current market rates in Dubai and Abu Dhabi:

| Service | Small Business (under AED 10M revenue) | Mid-Size (AED 10-50M revenue) | Large (AED 50M+ revenue) |

|---|---|---|---|

| Pre-audit health check | AED 5,000 – 15,000 | AED 15,000 – 35,000 | AED 35,000 – 75,000 |

| Full audit representation | AED 10,000 – 25,000 | AED 25,000 – 60,000 | AED 60,000 – 150,000+ |

| Voluntary disclosure filing | AED 3,000 – 8,000 | AED 8,000 – 20,000 | AED 20,000 – 50,000 |

| Reconsideration/TDRC appeal | AED 5,000 – 15,000 | AED 15,000 – 40,000 | AED 40,000 – 100,000+ |

Compare these costs against the penalties you face without professional support: a AED 500,000 tax difference discovered by the FTA costs AED 75,000 in the fixed penalty alone, plus AED 5,000 per month. Professional audit support at AED 10,000-25,000 for a small business is a fraction of the penalty exposure.

How Long Can the FTA Go Back in a Tax Audit?

Article 46 of Federal Decree-Law 28 of 2022 sets clear time limits on how far back the FTA can audit:

| Situation | Time Limit | Extension |

|---|---|---|

| Standard audit | 5 years from end of relevant tax period | 4 more years if audit notice sent before 5-year expiry |

| Voluntary disclosure in year 5 | 5 years + 1 year from disclosure date | None |

| Tax evasion | 15 years from end of relevant tax period | None specified |

| Failure to register | 15 years from date registration was required | None specified |

For corporate tax, the first tax period for most UAE businesses was June 2023 onwards. This means the FTA can audit your first CT period until at least June 2028 under the standard five-year rule. If you fail to register, the 15-year clock applies.

What Happens if You Disagree with the FTA’s Audit Assessment?

The Tax Procedures Law provides a structured dispute resolution path with strict deadlines. Missing any deadline means losing your right to challenge the assessment.

Option 1: Tax Assessment Review Request (Article 28)

Submit a written request to the FTA within 40 business days of receiving the Tax Assessment. The FTA must review and respond within 40 business days. This is the fastest route and keeps the dispute within the FTA.

Option 2: Reconsideration Request (Article 29)

If the review decision is unfavourable, submit a reconsideration request within 40 business days of the review decision. The FTA must respond within 40 business days. You cannot file both a review and a reconsideration simultaneously.

Option 3: Tax Disputes Resolution Committee (TDRC)

If the reconsideration fails, appeal to the TDRC under Article 30. The TDRC is an independent committee that reviews the FTA’s decision. Beyond the TDRC, you can appeal to the competent court.

Each stage requires detailed technical submissions referencing specific law articles, FTA public clarifications, and supporting documentation. This is where a registered tax agent provides the highest value: they know the legal arguments that carry weight and the precedents from previous TDRC decisions.

Should You Hire a Tax Agent Before or After the Audit Notice?

Before. Always before. Here is the financial comparison:

| Timing | What Happens | Cost Impact |

|---|---|---|

| Before audit notice (proactive) | Tax agent reviews returns, finds errors, files voluntary disclosure | 1% per month on tax difference only (no 15% fixed penalty) |

| After audit notice but before audit starts | Tax agent can still file voluntary disclosure, but the 15% penalty may apply if FTA has already flagged the issue | 15% fixed penalty may still apply + 1% per month |

| During or after the audit | FTA discovers errors directly; you face full penalties | 15% fixed + 1% per month + potential AED 20,000 non-cooperation |

For a business with a AED 200,000 tax error over two years, the difference between proactive disclosure and FTA discovery is approximately AED 30,000 in avoided fixed penalties. The cost of a pre-audit health check (AED 5,000-15,000) pays for itself multiple times over.

What Records Must You Keep for an FTA Audit?

Cabinet Decision 74 of 2023 specifies the record-keeping requirements. Failure to maintain proper records triggers a AED 10,000 penalty for the first violation and AED 20,000 for repeat violations within 24 months (Clause 1 of CD 75/2023).

- Accounting records and commercial books for 5 years from the end of the relevant tax period

- Real estate records for 7 years from the end of the calendar year

- Records related to an ongoing audit: retain for an additional 4 years

- Records related to a dispute: retain for an additional 4 years or until the dispute is finally settled, whichever is later

- All records must be organised to allow the FTA to verify tax obligations through a series of auditable documents

Frequently Asked Questions

How much notice does the FTA give before an audit?

The FTA must give at least 10 business days’ written notice before conducting a tax audit (Article 16, Clause 2 of Federal Decree-Law 28 of 2022). The only exceptions are suspected tax evasion, obstruction risk, or refusal to allow entry after proper notice.

What is the penalty for not cooperating with an FTA auditor?

A fixed penalty of AED 20,000 applies for failure to cooperate with or facilitate the Tax Auditor during an audit (Clause 12 of Cabinet Decision 75 of 2023). This penalty is charged to the person, their tax agent, or their legal representative from their own funds.

How far back can the FTA audit my tax returns?

The standard limitation period is 5 years from the end of the relevant tax period (Article 46, FDL 28/2022). For tax evasion or failure to register, the FTA can go back 15 years.

Can I represent myself during an FTA audit?

Yes, you can represent yourself. However, the FTA auditor will ask detailed technical questions about your accounting treatments, tax positions, and supporting documentation. Without tax expertise, you risk triggering additional scrutiny, making admissions that increase penalties, or failing to assert defences you are legally entitled to.

What is the difference between a tax assessment review and a reconsideration?

A Tax Assessment Review (Article 28) is the first step, filed within 40 business days of the assessment. A Reconsideration Request (Article 29) is the second step, filed within 40 business days of the review decision. You cannot file both simultaneously. Both have 40-day FTA response windows.

How many FTA audits were conducted in 2024?

The FTA conducted 93,000 inspection visits in 2024, a 135% increase compared to 2023. With corporate tax filing now live and the first deadline approaching in September 2026, audit volumes are expected to increase further in 2025 and 2026.

Is voluntary disclosure better than waiting for an FTA audit?

Significantly. Voluntary disclosure before an audit notice carries only a 1% per month penalty on the tax difference. If the FTA discovers the same error during an audit, you face an additional 15% fixed penalty on the entire tax difference (Clause 11 of Cabinet Decision 75 of 2023). On a AED 500,000 difference, that is AED 75,000 saved.

Can the FTA re-audit a tax period they already audited?

Yes. Article 19 of the Tax Procedures Law allows the FTA to audit any previously audited matter if new information surfaces that might impact the outcome, subject to the statute of limitations under Article 46.

Need Expert FTA Audit Support?

Qaspro Global’s tax consultants provide end-to-end FTA audit support: pre-audit health checks, document preparation, auditor liaison, voluntary disclosure filing, and dispute resolution through reconsideration and TDRC appeals. If you have received an FTA audit notice or want to prepare before one arrives, contact us today for a free consultation, or message us directly on WhatsApp.

For a full breakdown of the legal requirements, see our guide on bookkeeping compliance under UAE federal law.

Related Reading

- 7 Corporate Tax Red Flags That Trigger an FTA Audit in UAE 2026

- Why Hire a Tax Consultant Before an FTA Audit in UAE 2026

- Got an FTA Penalty? The 40-Day Reconsideration Window UAE 2026

- UAE Corporate Tax Penalties 2026: Every FTA Fine That Can Hit Your Business

- UAE Tax Penalties Change on 14 April 2026: What Every Business Must Do Now

- Best Tax Consultant Dubai 2026: What the Wrong Choice Costs You

- How Much Does a Tax Consultant Cost in Dubai 2026?

- UAE Corporate Tax Deductible Expenses 2026: Complete Guide

- UAE CT Filing September 30: File Now or Pay AED 500 Per Month

- How Did UAE Tax Procedures Change on 1 April 2026?

- Monthly Bookkeeping Checklist UAE 2026: Stay FTA-Compliant

- UAE External Audit Requirements 2026: Who Must Audit