What Is a VAT Voluntary Disclosure in the UAE and When Do You Need One?

Quick Answer: A UAE VAT voluntary disclosure is a formal correction, submitted as Form 211 on the EmaraTax portal, that you file when you find an error or omission in a VAT return you have already submitted. Under Article 10 of Federal Decree-Law No. 28 of 2022, if the error means you underpaid VAT by more than AED 10,000, you must file the disclosure within 20 business days of becoming aware of it. Disclosing before the FTA notifies you of an audit avoids the 15% fixed penalty.

Every UAE business that files VAT returns will eventually make a mistake: an invoice booked in the wrong tax period, output VAT recorded against the wrong Emirate, input tax claimed twice, or a zero-rated export reported as standard-rated. The Federal Tax Authority does not expect perfection, but it does expect you to fix errors the correct way and on time. In this guide, Qaspro Global breaks down exactly when a voluntary disclosure is mandatory, when you can simply adjust your next return, how to file Form 211 on EmaraTax, and what the corrected 2026 penalty regime under Cabinet Decision No. 129 of 2025 will actually cost you.

What Does a VAT Voluntary Disclosure Actually Do?

A voluntary disclosure is a legally defined form, prepared by the Federal Tax Authority, through which a taxpayer notifies the Authority of an error or omission in a tax return, a tax assessment, or a tax refund application. It is the official mechanism for correcting the past, separate from your normal VAT return for the current period. Filing one tells the FTA, in writing, that you found a problem and are fixing it before they did.

The key principle is in Article 10 of Federal Decree-Law No. 28 of 2022 on Tax Procedures. A voluntary disclosure is not optional in every case. The law splits errors into those you must disclose and those you may disclose, and the difference decides whether ignoring the error becomes a violation. Getting this wrong is one of the most common reasons a clean business walks into an avoidable fine during an FTA tax audit.

When Must You File a VAT Voluntary Disclosure?

Under Article 10 of Federal Decree-Law No. 28 of 2022, a voluntary disclosure is mandatory when an error worked in your favour, and optional when it worked against you. The rules are precise:

- Underpaid VAT (mandatory): If a submitted return or a tax assessment was incorrect and the payable tax was calculated as less than it should have been, you must submit a voluntary disclosure. This is Clause 1 of Article 10.

- Over-claimed refund (mandatory): If a refund application resulted in a refund more than you were entitled to, you must submit a voluntary disclosure under Clause 2.

- Overpaid VAT (optional): If the error meant your payable tax was calculated as more than it should have been, you may submit a voluntary disclosure to recover the difference. This is your choice under Clause 3.

- Under-claimed refund (optional): If your refund was less than you were entitled to, you may submit a voluntary disclosure under Clause 4.

There is a hard stop. Under Clause 5 of Article 10, no voluntary disclosure may be submitted after 5 years from the end of the relevant tax period, except in cases of tax evasion, where the FTA retains extended powers. Qaspro Global advises businesses to review historic returns well before that window closes, because a missed correction inside the five years is far cheaper to fix than the same error found by an auditor.

The AED 10,000 Rule: Voluntary Disclosure or Just Fix the Next Return?

Not every small mistake needs a full Form 211. The Executive Regulation of the Tax Procedures Law, Cabinet Decision No. 74 of 2023, sets a clear monetary threshold that decides the route you take. The deciding figure is the amount of the tax difference, not the size of the invoice.

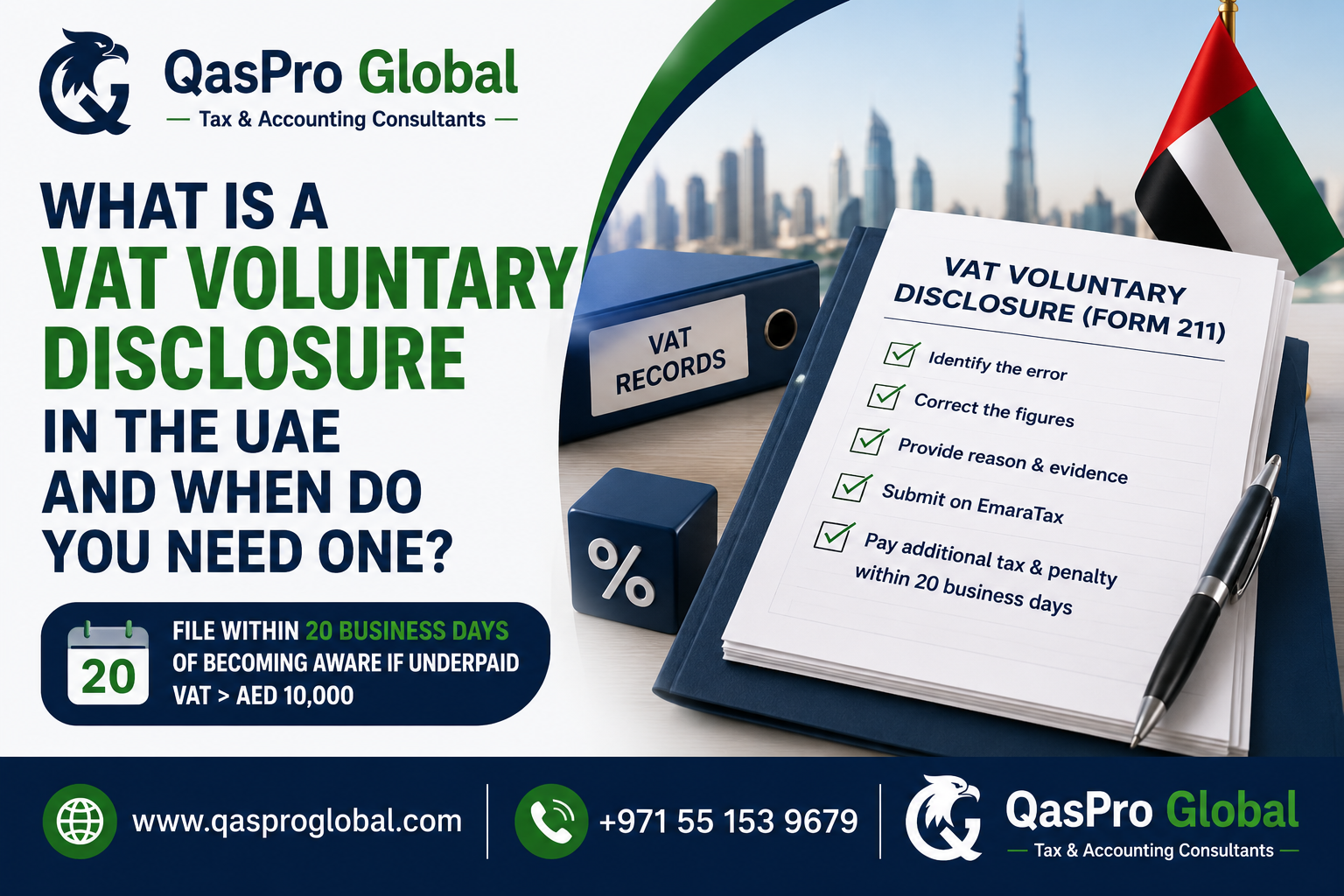

- Tax difference more than AED 10,000: You must submit a voluntary disclosure within 20 business days from the date you became aware of the error.

- Tax difference of AED 10,000 or less: If you are obligated to file a VAT return, you may correct the error in your next return instead of filing a separate disclosure. If you are not required to file a further return, you must submit a voluntary disclosure within 20 business days.

This threshold is the single most useful number for day-to-day VAT compliance. A AED 3,000 input tax error caught before your next VAT return filing can usually be cleaned up in that return with no separate form and no monthly penalty. A AED 40,000 understatement of output tax cannot, and the 20 business day clock starts the moment you discover it.

Do You Need a Voluntary Disclosure If There Is No Tax Difference?

Yes, in three specific situations, and this is where most businesses are caught off guard. FTA Decision No. 8 of 2024, effective from 1 January 2025, confirms that certain reporting errors require a voluntary disclosure even when the total VAT payable does not change at all. The three cases are:

- Wrong Emirate box: Reporting standard-rated taxable supplies for one Emirate in the box of another Emirate on the VAT return.

- Misreported zero-rated supplies: Incorrectly reporting zero-rated taxable supplies, whether you understated or overstated them.

- Misreported exempt supplies: Incorrectly reporting exempt supplies, whether understated or overstated.

These look harmless because the bottom-line tax is identical, but the FTA uses Emirate-level and supply-type data for its own reporting, so it treats these as correctable errors under Clause 5 of Article 10. The good news is that a voluntary disclosure with no tax difference does not attract the 1% monthly penalty, because there is no tax difference for the percentage to apply to. It is a compliance correction, not a financial one.

How to Submit a VAT Voluntary Disclosure on EmaraTax (Form 211)

The Federal Tax Authority processes all voluntary disclosures through the EmaraTax portal. The form is commonly known as VAT Form 211. Follow these steps:

- Log in to EmaraTax at the FTA portal and open the VAT account for the entity that filed the original return.

- Open the tax return you need to correct. Select the specific VAT period that contains the error, then choose the voluntary disclosure option against that return.

- Enter the corrected figures. EmaraTax shows the originally reported amount next to a field for the amended amount in each affected box. You only change the boxes that were wrong.

- State the reason for the disclosure. Provide a clear written explanation of what the error was and why it happened. This narrative matters: a vague reason invites questions.

- Attach supporting evidence. Upload invoices, credit notes, contracts, or a reconciliation schedule that proves the corrected figure is right.

- Review the calculated penalty and tax difference that EmaraTax displays, then submit the disclosure.

- Settle the additional tax and penalty within 20 business days. For a voluntary disclosure, the due date for payment is 20 business days from the date you submit the form. Pay through GIBAN or the EmaraTax payment options before that date to stop further late-payment penalties accruing.

Keep the disclosure reference and the payment confirmation. If a related reconsideration request becomes necessary later, that paper trail is your strongest evidence that you acted in good faith.

What Penalties Apply to a VAT Voluntary Disclosure in 2026?

The penalty regime that applies to corrections was restructured by Cabinet Decision No. 129 of 2025, effective from 14 April 2026, which amended the long-standing penalty schedule first set by Cabinet Decision No. 40 of 2017. The 2026 framework is built around the tax difference and around one decisive question: did you disclose before or after the FTA told you it was auditing you? This is the same shift covered in our guide to the April 14 2026 tax penalty change.

| Situation | Penalty (Cabinet Decision 129 of 2025) |

|---|---|

| Incorrect return, corrected within the filing deadline | No fixed penalty |

| Incorrect return, not corrected in time | AED 500 fixed penalty |

| Voluntary disclosure filed before any audit notice | 1% per month on the tax difference, from the day after the return due date until the disclosure is filed |

| No voluntary disclosure filed before the FTA audit notice | 15% fixed on the tax difference, plus 1% per month |

| Late settlement of the disclosed tax | 14% per annum on the unsettled tax, charged monthly from the day after the payment due date |

| Voluntary disclosure with no tax difference (FTA Decision 8 of 2024 cases) | No monthly percentage penalty |

The headline number is the 15%. Under the rules, if you fail to submit a voluntary disclosure for an error before the FTA notifies you of a tax audit, a fixed 15% penalty is applied on the tax difference on top of the 1% monthly charge. Voluntary disclosure is, quite literally, the difference between a 1% monthly cost and a 15% one-time hit.

Voluntary Disclosure Before vs After an FTA Audit Notice: A Worked Example

Consider a Dubai trading company that, in a 2026 review, finds it understated output VAT on a past quarterly return by AED 50,000. It became aware of the error roughly 4 months after that return was due.

Scenario A: the company files a voluntary disclosure now (before any audit notice).

- The error exceeds AED 10,000, so a voluntary disclosure is mandatory within 20 business days.

- Monthly penalty under Cabinet Decision 129 of 2025: 1% of AED 50,000 = AED 500 per month, for roughly 4 months = AED 2,000.

- It pays the AED 50,000 of underpaid VAT within 20 business days of filing to stop the 14% per annum late-payment penalty.

- Approximate total penalty cost: AED 2,000, plus the tax that was always owed.

Scenario B: the company does nothing and the FTA later issues an audit notice.

- Fixed penalty: 15% of AED 50,000 = AED 7,500.

- Plus the 1% monthly penalty for the period the error was outstanding.

- Approximate total penalty cost: AED 9,500 or more, plus the same underlying tax.

The voluntary disclosure saved this business around AED 7,500 in fixed penalties on a single error. Across several errors found in an audit, the gap between disclosing early and waiting becomes the difference between a manageable correction and a serious cash-flow event. This is why Qaspro Global treats a periodic VAT health check as risk management, not paperwork.

Common VAT Errors That Trigger a Voluntary Disclosure

Most disclosures come from a short list of recurring mistakes. Watch for these in your own records:

- Output VAT recorded against the wrong Emirate, a frequent issue for businesses with branches in more than one Emirate.

- Input tax recovered on blocked expenses such as entertainment or certain motor vehicles.

- Reverse charge entries missed on imports, the Box 3 reverse charge mistake that importers make most often.

- Standard-rated supplies treated as zero-rated exports without the required proof of export.

- Errors in input tax apportionment for businesses that make both taxable and exempt supplies.

- Bad debt relief claimed before the conditions and time limits were met.

Catching these against your accounting records before the FTA does is the entire value of a voluntary disclosure. Pair this review with your wider UAE tax deadlines calendar so corrections are planned, not panicked.

Frequently Asked Questions

What is a VAT voluntary disclosure in the UAE?

A VAT voluntary disclosure is an official Form 211 correction filed on the EmaraTax portal to fix an error or omission in a VAT return, tax assessment, or refund application that you already submitted. It is defined under Article 10 of Federal Decree-Law No. 28 of 2022 on Tax Procedures and is the legal way to correct the past before the Federal Tax Authority finds the error itself.

When must I file a VAT voluntary disclosure instead of fixing my next return?

You must file a voluntary disclosure when the tax difference is more than AED 10,000, within 20 business days of becoming aware of the error, under Cabinet Decision No. 74 of 2023. If the tax difference is AED 10,000 or less and you still file VAT returns, you may correct it in your next return instead. Errors that increased a refund or reduced the tax you paid are always mandatory to disclose.

How long do I have to submit a VAT voluntary disclosure?

You have 20 business days from the date you become aware of the error to submit the voluntary disclosure when the tax difference exceeds AED 10,000. Separately, no voluntary disclosure can be submitted at all after 5 years from the end of the relevant tax period, under Clause 5 of Article 10 of Federal Decree-Law No. 28 of 2022, except in cases of tax evasion.

What is the penalty for a VAT voluntary disclosure in 2026?

Under Cabinet Decision No. 129 of 2025, effective 14 April 2026, a voluntary disclosure carries a penalty of 1% per month on the tax difference, calculated from the day after the original return due date until the disclosure is submitted. If you fail to disclose before the FTA notifies you of an audit, an additional fixed penalty of 15% on the tax difference applies on top of the 1% monthly charge.

Is there a penalty if my voluntary disclosure has no tax difference?

No monthly percentage penalty applies when there is no difference in the VAT payable, because there is no tax difference for the 1% to be calculated on. FTA Decision No. 8 of 2024 still requires a disclosure for three reporting errors, namely a supply recorded in the wrong Emirate box, and incorrectly reported zero-rated or exempt supplies, even though the total tax is unchanged. It is a compliance correction rather than a financial penalty.

Can I get money back through a voluntary disclosure if I overpaid VAT?

Yes. Under Clause 3 of Article 10 of Federal Decree-Law No. 28 of 2022, if an error caused you to pay more VAT than you should have, you may submit a voluntary disclosure to correct it and recover the difference. This is optional rather than mandatory, but it is the correct route to claim back overpaid output tax or under-claimed input tax from a past return.

What happens if I do not file a required voluntary disclosure?

If you were required to disclose an error and did not, and the FTA discovers it during a tax audit, a fixed 15% penalty on the tax difference applies under Cabinet Decision No. 129 of 2025, plus the 1% monthly penalty and the underlying tax. Persistent or deliberate failures can also be treated as tax evasion under the Tax Procedures Law, which carries far more serious consequences than a standard correction.

How do I submit Form 211 on EmaraTax?

Log in to EmaraTax, open the VAT return for the period that contains the error, select the voluntary disclosure option, enter the corrected figures against the original amounts, state the reason for the change, attach supporting evidence such as invoices or reconciliations, and submit. You then settle any additional tax and penalty within 20 business days of submitting the disclosure to avoid further late-payment charges.

Does filing a voluntary disclosure trigger an FTA audit?

Filing a voluntary disclosure does not automatically trigger an audit, and it generally reduces your risk by showing the FTA you are correcting errors in good faith. The Federal Tax Authority can audit any registrant within the statutory time limits regardless, but a clean disclosure history and clear supporting evidence put you in a much stronger position if an audit does occur.

Need Expert Help With a UAE VAT Voluntary Disclosure?

Qaspro Global, a UAE-based tax and accounting consultancy, can review your past VAT returns, calculate the exact tax difference and penalty exposure, prepare and file your Form 211 on EmaraTax, and represent you with the Federal Tax Authority if questions arise. Whether you have found a single error or need a full historical VAT review before an audit, our tax consultants help you correct it the right way and on time. Contact us today for a free consultation.